|

|

|

|

|

|

General Robyn McLean 9 Jan

|

|

|

|

|

|

General Robyn McLean 9 Jan

Stay safe and enjoy the comfort of home this winter and all year long.

General Robyn McLean 3 Jan

What can Canadian home buyers and sellers expect as we enter a new decade? Check out Zoocasa’s top five predictions for home sales, price growth, and mortgage rates in the new year!

Canada’s housing market has come a long way from its 2016-2018 boom-bust cycle. After sustaining roughly two years of softer sales and price growth following the introduction of the federal mortgage stress test, as well as provincial taxes and policies in Ontario and British Columbia, demand for homes for sale found its footing in the second half of 2019.

Canada’s largest urban centres, such as the Greater Toronto Area and Greater Vancouver, as well as its strongest secondary markets, started to experience sustained rebounds in home buyer demand due to a number of factors, including lower interest rates; a subdued Bank of Canada (BoC), combined with strength in the bond market, kept the consumer cost of borrowing at historic lows all year long.

That’s helped soften the blow of the stress test, which requires insured mortgage borrowers to qualify at the Bank of Canada’s five-year benchmark rate, while uninsured borrowers must qualify for a rate roughly 2 percentage points higher than the one they’ll get from their bank. Not only did an overall lower rate environment pull the BoC’s qualifying rate down to 5.19% from 5.39% this year, but all borrowers enjoyed deeply discounted fixed mortgage rates, which outpriced even their variable counterparts at some of the nation’s most competitive lenders. With renewed purchasing power in hand, this drove buyers back into the market, causing year-over-year sales and price growth to spike in most of Canada’s major cities.

According to several real estate analysts and associations, home buyers and sellers can expect this trend to extend well into 2020. In its most recently revised forecast, the Canadian Real Estate Association expects the year to close out with 486,800 transactions, up 6.2% from 2018, before climbing to 530,000 sales next year, at an increase of 8.9%. The national average home price is expected to climb 2.3% to $500,000, and up 6.2% to $531,000 in 2020.

This optimistic outlook is echoed by the Canada Mortgage and Housing Corporation, which forecasts both sales and prices will “fully recover” from their recent declines, supported by growth in income among buyers, as well as population booms in Canada’s busiest job markets.

“Overall, economic and demographic conditions will remain supportive of housing activity over the forecast horizon, halting the declines in starts, sales, and average home prices that followed the highs of 2016 – 2017,” it states in its most recent Housing Market Outlook. Nation-wide, the CMHC expects 2020 sales to fall between 480,600 – 497,700 units, a year-over-year uptick of roughly 6%. The average price will fall between $506,200 – $531,000, up 5.6 – 6.7% from this year.

However, as has been the long-term trend, the strongest action will be seen in the Ontario and British Columbia markets, particularly in the latter as it recovers from a slew of foreign buyer and non-resident speculation taxes. BC sales are expected to jump a whopping 20 – 22.6% next year with 74,600 – 84,400 transactions, with prices up 2.8 – 3.6% at an average of $675,000 – $749,500, says CMHC.

In the Ontario real estate market, sales will hit between 204,200 – 213,800 units (+4.2 – 7.3%), with prices between $614,000 – $633,700 (+5.4 – 6.5%).

In contrast, overall volumes and growth will be much lower in the Prairie markets, where economic performance and spending power remain challenged by a downturn in the energy industry and housing markets are plagued by oversupply. In Alberta, 2020 sales will hit between 52,300 – 56,900 units (+4.1 – 4.2%), while prices will inch up to the $379,700 – $383,400 range (+1.9 – 2.9%). In Saskatchewan, sales are forecasted to reach between 10,800 – 11,200 (+3.8 – 5.6%), with prices between $275,100 – $283,900 (+0.5 – 1.5%).

Quebec, however, will continue to experience stable sales growth and faster-than average price surges; CMHC calls for a total of 91,500 – 96,500 transactions in 2020 (+0.3 – 2.5%), with the average price between $341,000 – $348,000 (+6.2 – 6.4%).

It’s no secret that market conditions in Canada’s largest cities have been largely defined by a growing supply and demand gap. While factors such as foreign and domestic investment have also contributed to too-hot-to-handle price growth, that there have been too few homes to satiate demand, particularly in the GTA markets, set the stage for bidding wars and a stratospheric rise in home values over the course of 2016. That infamously led to the implementation of the Ontario Fair Housing Plan, which included a number of measures including a foreign buyers’ tax and rent controls, to cool the demand end of the market.

For a time, these new policies were effective in chilling the market; combined with the federal mortgage stress test, the measures thoroughly spooked sellers, leading to a 33% drop in new listings following their announcement. As well, home prices plunged across the province, with York Region bearing the brunt with double-digit declines.

While sales and prices have rebounded steadily over the past year, the same can’t be said for new listings. From a national perspective, Canadian real estate as a whole could be considered a sellers’ market in November, with a sales-to-new-listings ratio of 66.3%, as new supply shrank by -2.7% year over year. As well, the total months of inventory – the length of time it would take to completely sell off all available homes for sale – currently sits at 4.7 months, its lowest level since 2007.

However, recent reports out of the GTA show that lack of supply is a far more acute issue. The end-of-year numbers from the Toronto Real Estate Board reveal the SNLR for the region was 81%, indicating just under 20% of all new listings brought to market were sold in November.

TREB’s analysts are raising concerns that should undersupply persist, it could set the stage for the type of unsustainable price growth seen in the 2016 market, which was what prompted new regulatory change in the first place.

“Strong population growth in the GTA coupled with declining negotiated mortgage rates resulted in sales accounting for a greater share of listings in November and throughout the second half of 2019,” says Jason Mercer, TREB’s chief market analyst. “Increased competition between buyers has resulted in an acceleration in price growth. Expect the rate of price growth to increase further if we see no relief on the listings supply front.”

The BoC – the national central bank that sets the cost of borrowing for consumer lenders – has kept mortgage interest rates relatively low and stable for the entirety of 2019, keeping its trend-setting overnight lending rate at 1.75% in each of its eight announcements. As a result, banks and credit unions were able to keep their variable mortgage and line of credit products competitively priced. As well, yields for national bonds, which lenders use to set the cost of fixed-rate borrowing, hit historic lows, indicating increased popularity with no imminent risk of a devaluing rate hike on the horizon.

Due to this, borrowers have had access to some of the lowest mortgage rates on record in 2019 – and this is likely to persist throughout the new year, according to the latest communications from the BoC. In the Bank’s year-end speech, Governor Stephen Poloz outlined the major long-term forces that will shape the economy and interest rates over the next year – and they look to stick to status quo.

Overall, the BoC will take to the same cautious stance it did in 2019; economic factors at home and abroad aren’t quite strong enough to warrant higher interest rates, but are stable enough to prevent a rate cut. Avoiding a cut also leaves some wiggle room in case global trade and recession risks do materialize, and the BoC needs to take action.

The BoC points to ongoing trade wars – and particularly tensions between the U.S. and China – as the biggest risk that could upend the global economy and stall growth. It also points out that slowing populations in many economies is holding back global output. “Because slow growth is likely to persist, interest rates will stay lower than usual,” the BoC states.

Other factors that make a rate hike less likely include the latest fiscal update from the federal government, which reveals there will be a $26.6-billion deficit recorded for 2019, and $28.1-billion expected in 2020. This, combined with Canada’s notoriously high levels of household debt, remain key vulnerabilities should the economy go belly up – and the BoC acknowledges that lower interest rates will help fuel irresponsible borrowing.

“When interest rates are low, households, firms and governments tend to borrow more. That supports the economy, but high debt means more vulnerability if something bad happens,” it states.

Another interesting development is renewed scrutiny for the aforementioned mortgage stress test – in December, a letter from Prime Minister Justin Trudeau indicated Federal Finance Minister Bill Morneau will take a second look at the controversial test’s criteria, and potentially make tweaks to allow for more flexibility when qualifying borrowers.

While no details have been released as of yet, this could include lowering the qualifying rate from its current 5.19%, or making it more dynamic based on individual borrowers’ profiles, As well, they could remove the current requirement for borrowers to be re-stress tested when switching lenders, a measure that has drawn heavy criticism from the mortgage industry for discouraging consumer empowerment and competitiveness.

General Robyn McLean 11 Dec

Moving during the winter holiday season might not be your first choice – or even your second – but, if you’re in this position, it’s probably because of some very serious reasons. Once the decision is made, it’s important to learn all about the particularities of moving during this pretty busy time of the year, what you should be paying extra attention to, and how you can actually benefit from the situation.

The winter holiday season conventionally spreads from Black Friday until New Year’s Eve, but there are several “peak days” during this time that you shouldn’t choose as your moving dates. Black Friday sees a huge amount of road traffic, so driving a rental truck on any of those days will be quite challenging. However, the weekend following Black Friday is a good choice, as the shopping madness subsides.

Avoid, for the same reason, the couple of days leading up to Christmas –from December 22ndto December 24th, when roads and airports are extremely busy. But if you’re planning a DIY move with a rented truck, the first and second Christmas Days might just be the winning bet – everyone’s at home, the roads are almost deserted, and you and your family have time off from work and school – but only if you don’t celebrate Christmas too much!

However, if you’re interested in hiring a moving company, you need to rethink the time frame. It’s unlikely you will find companies available to move you during Christmas or Boxing Day. However, excluding those celebratory days, a winter holiday season move might actually save you some bucks. Few people choose to move in November and December, due to weather, so moving companies are at their slowest and slashing prices.

Another silver lining of moving during this time of the year is that you’re probably having more days off than usual. It’s no fun to spend those days packing your home, but at least you have time to do it properly. Besides, you’ll be celebrating the New Year in your new home, which counts for something.

Make the most of your free days and jump-start your move. Sort through your things, decide what goes with you and what stays behind, and prepare the bulk of your stuff for moving.

If it’s a relatively short-distance move, for example from Philadelphia to New York City in the U.S., or from Toronto to Mississauga in Canada, you can even do it in stages, to ease the burden. For example, rent a self-storage unit and use it as your “moving base” – pack during your time-off, then make a few trips and store your stuff in there. Self-storage facilities have convenient schedules, and many are even open seven days a week, 24 hours per day –it’s easy to fit in some back-and-forth trips. By the time the actual moving day arrives, most of your belongings will already be at the destination, making the whole process a lot easier.

Moving also involves decluttering – and what better time of the year than this to donate the items you no longer need? Contact a charity organization and have them pick up your slightly worn things that are in high demand right now, such as winter clothing, books, toys, baby stuff and even furniture and electronics.

You could also donate your winter holiday decorations – it’s unlikely you’ll have the time for a fully decorated home this year, so why not spread the cheer and give them to someone who would truly appreciate them?

If you’re planning to buy new furniture, electronics, or appliances for your new home, you’re in luck, and you’ll probably score some great deals. Black Friday, Cyber Monday, and Christmas sales await you – we’re talking about weeks of special offers and discounted prices.

Check out the offers and do the math – is it worth it to pack and transport your furniture and appliances? Moving large items is usually the most expensive part of a move – maybe you’re better off leaving them behind and getting new items at your destination.

Hold on to the cheer! You’re moving during the holiday season, but that doesn’t mean you can’t still have fun. You might not have the time, energy, or money for a full-blown holiday season, with dinner parties, gifts, and decorations. But you’re spending time with your family – a lot more than usual, for sure – and that’s the most important part. Christmas on the road? Well, you can make it memorable by packing a goodie basket and small gifts for everyone, and by playing family road-trip games.

Planning ahead and making the most of every opportunity this special time of the year provides will help you manage your winter holiday season move – and maybe it’s not going to be nearly as bad as you initially feared!

General Robyn McLean 11 Dec

The First-Time Home Buyer Incentive (FTHBI) was launched on September 2, 2019 by the federal government and offers a 5% or 10% contribution towards your down payment in the form of a shared equity mortgage. The program aims to improve affordability by reducing the monthly mortgage payments for buyers.

There is no interest charged on the FTHBI amount nor is there an ongoing repayment schedule, instead the government will share in the upside and downside of the property value. The FTHBI offers the following down payment contributions:

Only residential properties in Canada that are suitable for full-time, year-round occupancy are eligible. The property must be intended for the homebuyers’ own occupancy and investment properties are not permitted.

Examples of residential properties include:

Buyers who wish to participate in the First-Time Home Buyer Incentive program must meet the following criteria:

For the purpose of the FTHBI, you are considered a first-time home buyer if you meet any of these qualifications:

Minimum down payment and mortgage requirements for the FHTBI:

In addition, the closing date for a re-sale home must be within 6 months from the application approval. The closing date for new a construction home must be within 18 months from the application approval.

The maximum price you could buy a home for under the FTHBI depends on your qualifying income as well as your down payment.

Here is a sample maximum home price calculation:

Suppose your annual qualifying income is $120,000/year (the maximum allowable when using the FTHBI). The FTHBI stipulates the maximum amount you can borrow, including the FTHBI amount, is four times your income, thus you can borrow up to $480,000 to purchase a home.

i. Maximum home price if you have the minimum down payment of 5%

The minimum down payment required from the home buyer is 5%, thus the maximum price of a re-sale home you could purchase is $505,263 (calculated as $480,000 divided by 0.95).

ii. Maximum home price if you have a down payment of 14.99%

With a down payment of 14.99%, the maximum price of a re-sale home you could purchase is $564,639 (calculated as $480,000 divided by 0.8501).

The home buyer must repay the FTHBI amount in full after 25 years or when the property is sold, whichever comes first. The full amount can be repaid in full anytime, without a pre-payment penalty; however, partial repayments are not permitted.

The amount due to be repaid is calculated as the percentage of the FTHBI times the home’s value at the time of repayment. For example, if a homebuyer received 5% of the down payment through the FTHBI at the time of purchase, the homebuyer will repay 5% of the home’s fair market value at the time of the repayment.

Here is a sample repayment calculation:

You purchase a property for $400,000 and receive a 5% for your down payment through the FTHBI in the amount of $20,000. When you sell your home within 25 years, the home value has increased to $600,000. The repayment amount due would be 5% of $600,000, or $30,000.

To apply for the FTHBI, complete the application documents found on the official First-Time Home Buyer Incentive Plan website, speak to your mortgage lender and notify the lawyer who will be managing your home closing.

General Robyn McLean 4 Dec

Valuable insight on the BoC rate hold announced today, from our Chief Economist, DR. Sherry Cooper.

|

|

|

|

|

|

General Robyn McLean 3 Dec

Wow…there’s some discouraging data here however it certainly puts Vancouver’s ongoing affordability issues into clear light. It also emphasizes that saving for a down payment should start as early as possible. Great article from Zoocasa!

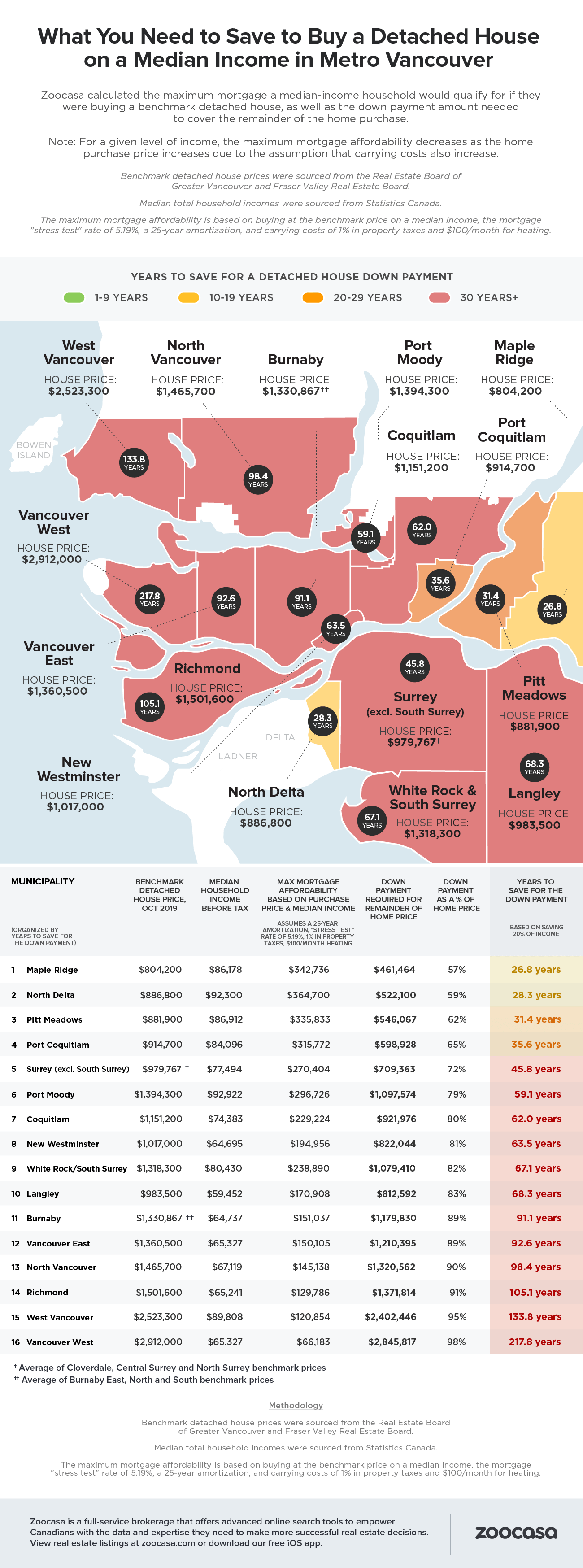

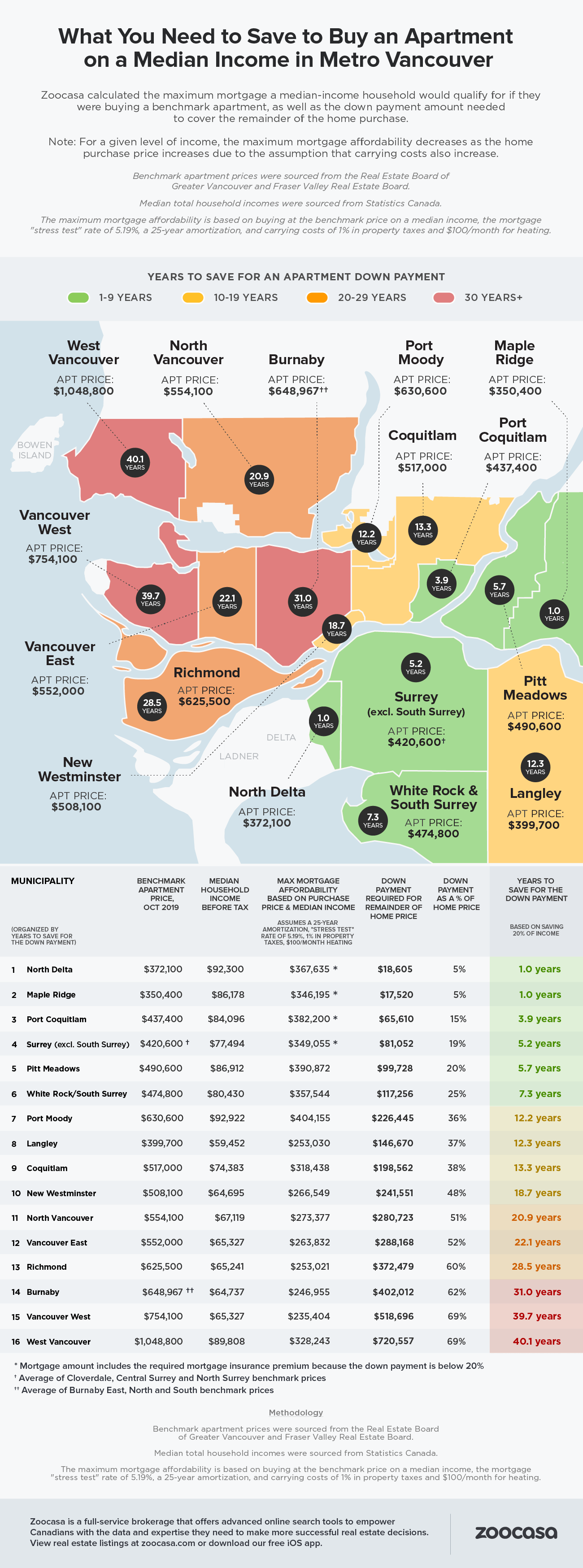

NOVEMBER 21, 2019

The Metro Vancouver housing market has long held the notorious distinction of being the priciest in Canada; steeply rising home prices and fears of speculative activity have prompted action from both the provincial and municipal governments in recent years, including a foreign buyers’ tax, empty-homes tax, as well as a levy on homes owned by those who do not pay income tax in the province.

And it would appear these measures have been somewhat effective; combined with the federally-implemented mortgage stress test, these taxes have chilled sales, price growth, and MLS listings in Vancouver over the last two years. While buyers are now starting to return to the Vancouver market, prices still remain below year-ago levels: according to the Real Estate Board of Greater Vancouver, the benchmark home price for all residential properties hit $992,900 in October, down -6.4% year over year. Detached houses now fetch a benchmark of $1,410,500, a decline of -7.5%, while apartments cost $652,500, down -5.9%.

However, despite improved affordability in the Vancouver market, has the property ladder become any more accessible to middle-class buyers? How feasible would it be for a household with the median income to afford the benchmark-priced home in their local municipality?

To find out, Zoocasa sourced benchmark home prices for both detached houses and apartments in 16 municipalities across Metro Vancouver. The study then calculated the maximum mortgage amount a median-income household in that city would qualify for if they were purchasing the benchmark home in their region. The study then calculated the remaining required down payment, as well as the timeline required to save those funds, assuming households put away 20% of their income each year.

Mortgage calculations were based on the federal mortgage stress test rate of 5.19% and a 25-year amortization, as well as carrying costs of 1% for property taxes, and $100 monthly for heating bills.

Based on the findings, there are no municipalities in which a median-income household could afford Metro Vancouver houses for sale without having to save for at least two decades for the necessary down payment. In fact, in the three priciest luxury neighbourhoods including Richmond, Vancouver West, and West Vancouver, where benchmark home prices range between $1.5 – $2.9 million, it would actually take more than 100 years to come up with the needed funds.

While this isn’t a realistic scenario for home buyers – those facing such a gap between their mortgage qualification and desired home purchase would instead seek out housing options better aligned with their incomes – the numbers reveal just how large the disparity is between median-income household affordability and home prices in some Metro Vancouver municipalities.

Even municipalities with comparatively more affordable detached house benchmark prices were far beyond reach for median-income earners; in Maple Ridge, North Delta, and Pitt Meadows, where benchmark house prices range between $804,200 – $881,900, home buyers would need to save between 27 – 32 years to amass the necessary down payment.

The good news is that there are still several municipalities that offer affordable entry-point housing for median-income earners; those looking to purchase Vancouver condos could hope to do so on a savings timeline of less than five years in North Delta, Maple Ridge, and Port Coquitlam, where the benchmark price ranges from $372,100 – $437,400.

However, those looking to purchase multi-family housing won’t find many entry-level options in the region’s most expensive markets; with benchmark prices between $648,967 – $1,048,800, it would take between 31 – 40 years to save a down payment large enough to purchase a unit in Burnaby, Vancouver West, and West Vancouver.

1 – Maple Ridge

2 – North Delta

3 – Pitt Meadows

1 – Vancouver West

2 – West Vancouver

3– Richmond

1 – North Delta

2 – Maple Ridge

3 – Port Coquitlam

1 – West Vancouver

2 – Vancouver West

3 – Burnaby

Methodology

Benchmark detached house and apartment prices were sourced from the Real Estate Board of Greater Vancouver and Fraser Valley Real Estate Board.

Median total household incomes were sourced from Statistics Canada.

The maximum mortgage affordability is based on buying at the benchmark price on a median income, the mortgage “stress test” rate of 5.19%, a 25-year amortization, and carrying costs of 1% in property taxes and $100/month for heating.

General Robyn McLean 3 Dec

The Canadian economy continues to stubbornly support the Bank of Canada’s interest rate policy. Market watchers are pretty much unanimous in their projections that the central bank will stay on the sidelines, again, when it makes its rate announcement later this week.

The latest numbers from Statistics Canada show gross domestic product grew by 1.3% in the third quarter. That is a slow down, but it is a long way from anything that would trigger BoC intervention. Consumer spending and housing are seen as the main drivers of that growth.

Housing has recovered nicely from its sluggish performance earlier this year and it would seem that the market has made a soft landing. But the Bank continues to worry that lowering interest rates could spark another round of debt-fueled buying. In the Bank’s opinion, high household debt remains a key vulnerability for the Canadian economy.

Of course an interest rate cut would weaken the relatively strong Canadian dollar which is hampering the export sector, but the Bank has said it would like to see other methods used to encourage exports and business investment. Even lower interest rates and a weaker Loonie might not be enough to push through the international economic headwinds created by the current spate of tariff and trade wars that have slowed global growth.

Now the forecasters are looking as far ahead as the second quarter of 2020 before they see any interest rate activity. By then we should being seeing the effects of the U.S. presidential election campaign.

Dec 2, 2019

First National Financial LP

General Robyn McLean 27 Nov

You may not think about your roof and gutters very much, if at all. But it’s important to give them a checkup and some TLC to prevent big problems down the road.

General Robyn McLean 26 Nov

Some great tips for keeping your family & home safe this winter from our friends at PillarToPost!

We hope you enjoy a happy and safe holiday season!