A valuable outline from our friends at Planswell to help you reach your home ownership goals!

While it doesn’t always make sense for everyone, home ownership is often a financial goal for many Canadians. It can be the ideal setting to raise a family, build wealth in equity, or set yourself up for retirement.

A recent Globe and Mail feature shed some good news “that roughly three-quarters of Canadians live in communities where home ownership is affordable.” But no matter where you live or how much the average house price is, there are certain steps you need to work through on your journey to home ownership.

Before charging ahead, be honest with yourself if owning a home makes sense for your life goals and plans. If it does, then keep reading – we’ve broken it down in a step by step list for how to get you to your home ownership goal:

Establish how much you can afford

Once you’ve decided that all of the responsibilities that come along with home ownership is the right direction for you, start by taking a hard look at your finances.

Make sure your credit score is in tip-top shape while you’re establishing how much you can afford. “Ensure your credit score is in tip top shape leading up to getting preapproved. No late payments, try to minimize the amount owing, don’t take out any new credit,” said Planswell Mortgages’ Samson Tella.

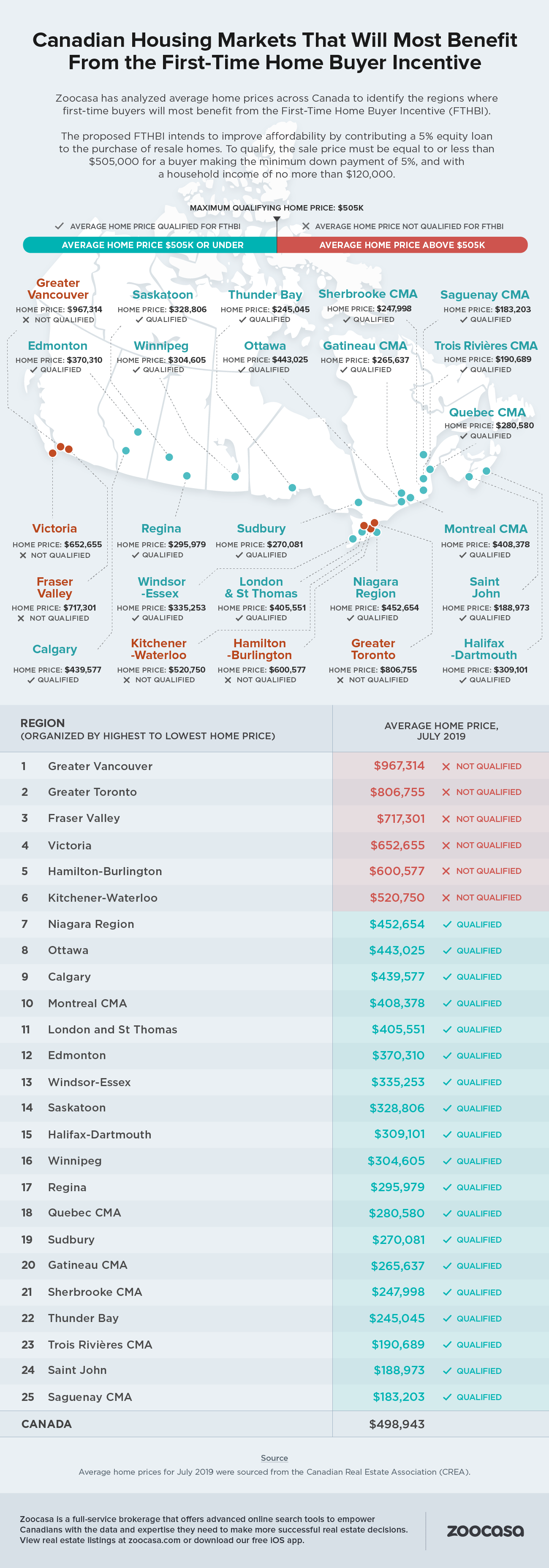

Do some market research and figure out where you want to live

Establishing how much you can afford may provide some direction when it comes to where you want to look. Every town and city is different, but they’ll all have areas that are considered more desirable and you’ll see that reflected in the price.

Our advice? Sometimes the greatest gem is hard to see at first. Be open to fixer-uppers that you can build into your dream home out of and you’ll often see a greater financial return over time.

Get pre-approved for a mortgage

Because you’ve been focused on maintaining a tip-top credit score since the time you started to establish what you can afford, the pre-approval process will be a lot smoother.

Another aspect to consider before you are in search of your pre-approval is the stability of your income. Don’t change careers when you’re looking to purchase a home. Lenders aren’t very friendly when looking at applicants that are still in that probationary period.

If you have a fluctuating income, a lender will want to look at a two-year running average so have your notice of assessments ready if you want to qualify for more than your base hours/salary. This includes OT/Bonuses/Car Allowances/Etc.

Don’t forget to disclose any additional factors that may help you get pre-approved. Have a lot of liquid assets? Have a cosigner? Have a side hustle that you claim on your taxes? Let your mortgage broker know. The clearer the picture your mortgage broker has, the stronger of a case they can make to get you approved for a mortgage that is right for you.

Establish your down payment

When it comes to down payments, minimums are required. You’ll need 5% of the purchase price for homes valued under $500,000 and 10% of the balance above $500,000 up to $1,000,000 purchase price. For homes with a purchase price over $1,000,000, you’ll need at the very least 20% down, if not more, depending on the lender.

How are you going to get there? Save, save, save

This is where a strict budget comes in handy. Try out our monthly budget calculator and try to be as strict with your spending as you can. Keep in mind that you have a goal you’re working towards, and you’re only going to get there by changing the way you’ve been doing things when it comes to your spending.

Once you have that down payment all ready and saved up, don’t be moving it around to different accounts – especially not locked in accounts like an RRSP. Sure, if you’re a first-time home buyer the RRSP Home Buyers’ Plan may be a fit for you, but there are many stipulations like the funds have to have been in the RRSP for at least 90 days. Check out this article to learn more about the ins and outs of the RRSP Home Buyers’ Plan.

Find that dream home (or as close to as possible!)

Now that you know how much you’re going to be putting down, and you have a target price you’re able to afford you can narrow in on where you can look for that dream home.

It’s often recommended not going to your maximum mortgage amount when you’re looking for your home. There are often things you forget when going from a renter to a home buyer: legal fees, property taxes, condo fees in some cases, water heater rentals, association fees… I could go on and on here.

Basically, don’t go crazy here – stay well within your budget to ensure that you’re not feeling stretched thin when it comes to all of the new expenses you’re about to incur with being a homeowner.

You can sometimes expect to pay 1.5% – 3.0% of the value of the home in other fees on the day of closing. This includes tax on the CMHC premium (if applicable), property tax, and many other fees. For example, if you’re purchasing a $700,000 house you can expect to pay around $20,000 in fees on the closing date.

Secure your mortgage

After you’ve placed your “offer to purchase”, your next step is to contact your mortgage broker to get your mortgage approval. Your mortgage broker can help you here, but you’ll also need a lawyer for their assistance.

Once you’ve secured your mortgage, you need to fulfill the mortgage and legal requirements to fund your mortgage as scheduled to ensure your plan goes off without a hitch. This looks different depending on what lender your mortgage is coming from, but don’t worry – your mortgage broker should hold your hand through this process to make sure you don’t miss any steps.

Well, there you have it: a step-by-step guide to your journey from being a renter to a homeowner. While this is an overview and there are of course many more in-depth aspects to each part of your journey, there is one overarching theme here that will determine your success as a homeowner: having a financial plan.

By Lauren Arnold, Planswell

JULY 28, 2019