1. Possible Tax Breaks and Benefits are Attractive Incentives

Everyone loves a tax break! Although most tax benefit programs are specific to each province, there is a National Program called the First-Time Home Buyers’ Tax Credit (HBTC). The purpose of the HBTC is to give you back a small portion of the purchase price considering that one of the biggest challenges for first-time home buyers is the down payment. This tax credit can give you a non-refundable $5,000 when you file your tax return the year after you purchase. This translates to roughly $750 extra in your pocket. Great for those new home expenses that may pop up.

Provincially, there are many different tax breaks and benefit programs available across the country. Exclusive to British Columbia, for example, is the First Time Home Buyers’ Program. It exempts first-time home buyers from the property transfer tax by reducing or eliminating the amount of tax paid. There are certain stipulations so make sure you check the qualification criteria

BC has some of the most expensive real estate in the country, and with that comes some of the steepest property taxes. With the Home Owner Grant, you may be eligible to reduce property taxes on an annual basis with the amount of tax relief dependant on where you live. For example, if you are living in Vancouver you might be eligible for a $570 grant, whereas outside of the Capital Regional District, Greater Vancouver, or the Fraser Valley District, you may be eligible for a grant of $770.

BC also has a tax incentive for home buyers who are not first-time home buyers necessarily but are purchasing a newly built home. The Newly Built Home Exemption helps lower or eliminate the property transfer tax you are required to pay. This exemption applies to newly built homes only and can save you up to $13,000 in tax exemptions.

Similarly, Ontario offers a refund on all or part of your land transfer tax. But you need to be an eligible first-time home buyer. This program can save you up to $4,000 in taxes. Prince Edward has a program as well with a maximum of $2,000 refund.

2. How Canada Mortgage and Housing Corporation Helps with Home Ownership

Canada Mortgage and Housing Corporation (CMHC) is a Crown Corporation of the Government of Canada. It exists to help make housing affordable to everyone in Canada and has developed several programs to help homeowners and first-time home buyers find more affordable options.

The First-Time Home Buyers Incentive Plan offers five to 10 per cent of the homes’ purchase price to put toward a down payment. These additional funds added to your down payment help lower your mortgage carrying cost.

The Government of Canada, essentially, partners with you in a Shared Equity Mortgage, taking a share of the increase or decrease in your property’s market value. There are specific criteria to qualify.

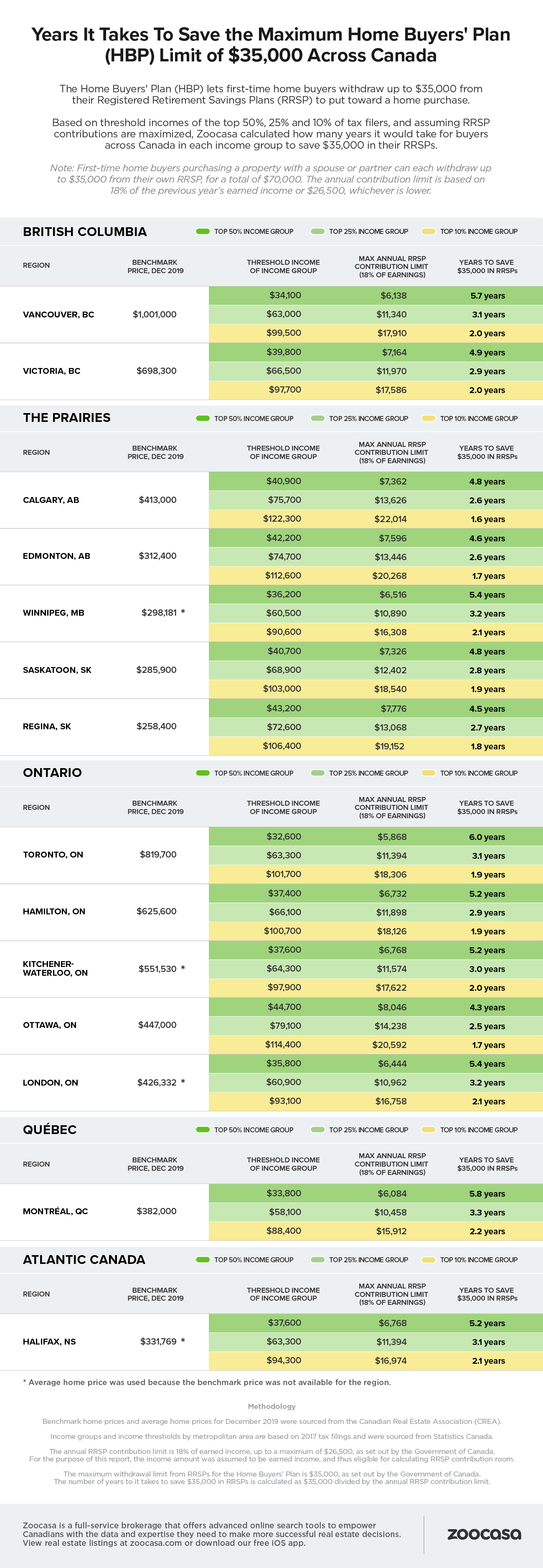

3. Home Buyers Plan Helps You Leverage RRSP Investment

Another great Federal Program is the Home Buyer’s Plan (HBP), which allows you to use a $35,000 Registered Retirement Savings Plan (RRSP) withdrawal to put towards your new home purchase. It is specifically designed to assist first-time home buyers in saving funds to purchase a home.

Normally, when you withdraw funds from your RRSP, you’re taxed on those funds. Under the HBP, you can withdraw up to the $35,000 amount in a single calendar year to put towards a down payment of your first home.

4. GST/HST New Housing Rebate Can Put Money Back in Your Wallet

It’s true! By buying a home you may qualify for a rebate on part of the GST or HST you paid on the purchase or cost of building your new home. In addition, you could save on the cost of substantially renovating or building a major addition onto your existing home, or on converting non-residential property into a house. There are multiple rebates you can claim, and the value of this rebate will vary based on which category your home purchase falls. Your accountant or tax office can point you in the right direction on this one.

5. Building Equity and Credit Gives Financial Benefits

Beyond the provincial and federal programs available, another key financial benefit to buying a home is to build equity. Not only will you own “more” of your home (a.k.a. equity), you also build a line of credit. This is a significant asset you can use for almost anything. A home equity line of credit (HELOC) is essentially a secured form of credit. The lender uses your home as a guarantee that you’ll pay back the money you borrow. You can borrow money, pay it back, and borrow it again, usually up to a maximum credit limit.

If you have been renting because home ownership seemed out of reach, look at the requirements to qualify for these programs. You may be surprised at what you can save as a homeowner!

By Catherine Musgrove Jan 22, 2020

Rew.ca