The Covid-recovery…insight and future outlook for our Canadian economy by Dr. Sherry Cooper, Chief Economist for Dominion Lending.

|

|

|

General Robyn McLean 9 Jul

The Covid-recovery…insight and future outlook for our Canadian economy by Dr. Sherry Cooper, Chief Economist for Dominion Lending.

|

|

|

General Robyn McLean 18 Jun

Current housing market review by Dominion Lending’s Dr. Sherry Cooper.

|

|

|

|

|

|

|

|

|

|

General Robyn McLean 11 Jun

Insight on the latest Bank of Canada announcement from our friends at First National.

This morning, in its fourth announcement of 2021, the Bank of Canada left its target overnight benchmark rate unchanged at 0.25%. As a result, the Bank Rate stays at 0.5%. It also provided somewhat encouraging thoughts on the state of, and outlook for, the Canadian and global economies and updated its outlook on inflation. Here is a summary:

Canadian economic conditions

Inflation

Global conditions

Looking forward

Despite progress on vaccinations, there continues to be uncertainty about the evolution of new COVID-19 variants. However, with provincial containment restrictions on an easing path over the summer, the Bank still expects the Canadian economy to rebound strongly, led by consumer spending. Growth in foreign demand and higher commodity prices should also lead to a solid recovery in exports and business investment, according to the Bank.

With respect to the housing market, the Bank’s only comment was that “activity is expected to moderate but remain elevated.” In April, the Bank opined that housing construction and resales were at historic highs, “driven by the desire for more living space, low mortgage rates, and limited supply” and noted that it would continue to monitor the potential risks associated with the rapid rise in house prices.”

Policy measures

The BoC’s Governing Council noted that there remains considerable excess capacity in the Canadian economy, and that the recovery continues to require “extraordinary monetary policy support.”

Accordingly, the Bank said it remains committed to holding its policy interest rate at what it calls the effective lower bound until economic slack is absorbed and its 2% inflation target is “sustainably achieved.” This may happen sometime in the second half of 2022.

As well, the Bank reiterated that it would continue its Quantitative Easing program – at a target pace of $3 billion per week – to keep interest rates low across the yield curve. It also added that: “Decisions regarding adjustments to the pace of net bond purchases will be guided by Governing Council’s ongoing assessment of the strength and durability of the recovery. We will continue to provide the appropriate degree of monetary policy stimulus to support the recovery and achieve the inflation objective.”

The bottom line

Today’s announcement falls under the heading no news is good news. The benchmark rate is unchanged, the economic recovery appears to be unfolding largely as expected and bond buying activity will continue to provide monetary policy support in the near term.

All of this suggests now is a good time to borrow but also with a view toward developing mid to long-term financing strategies that will address future conditions including the potential for policy interest rate increases next year.

General Robyn McLean 7 Jun

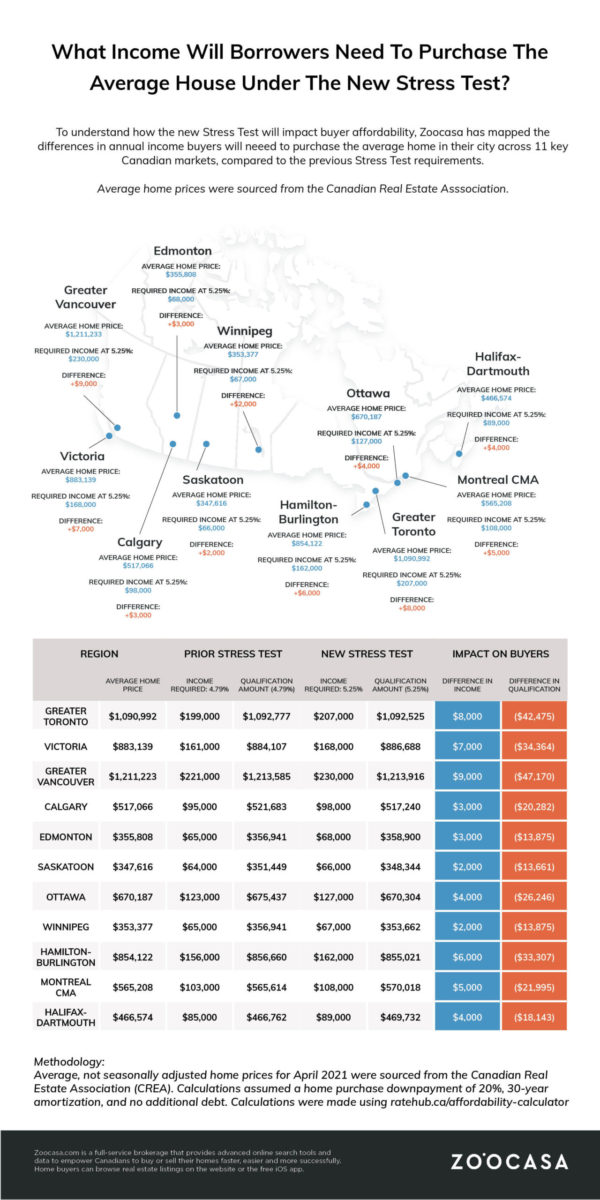

Some great insight on the increase of the stress-test in Canada from our friends at Zoocasa.

As of today, it’ll be a bit tougher for new and renewing mortgage borrowers to qualify for their home loan. A higher threshold for the “stress test” has come into effect, requiring borrowers to prove they can carry their mortgage costs at an interest rate of 5.25% or their contract rate plus 2%, whichever is higher. This is a slight increase from the previous threshold of 4.79%. The stricter criteria applies to both insured mortgage borrowers (those who make a down payment smaller than 20% on their home purchase) and uninsured borrowers, who put down 20% or more.

Simply put, in order to pass the stress test, borrowers must have healthy-enough incomes and debt servicing ratios to indicate they could pay their mortgage payments at the higher interest rate, regardless of the rate they actually get from their lender. For context, current fixed and variable mortgage rates are as low as 1.7% – 2% for a five-year term, so the stress test will tack on at a minimum 3% or higher. This translates to borrowers qualifying for a smaller mortgage amount.

However, as borrowers have been stress tested since 2018, the impact of this latest change will be fairly minimal. According to analysis conducted by Zoocasa, a buyer looking to purchase the average-priced home in their city would face a dip in affordability of about 3.8%, with between $14,000 – $47,000 shaved off the amount they’d qualify for. To make up for this difference, the study determined borrowers would need to supplement their incomes between $2,000 – $9,000 in order to qualify for the same size mortgage under the new stress test, depending on the city they’re purchasing in.

To determine these differences, Zoocasa calculated the income required to qualify for a mortgage large enough to purchase the average-priced home in 11 cities across Canada at both a mortgage rate of 4.79%, and then at 5.25%. It was assumed home buyers had no additional debt, were making a 20% down payment, and were amortizing their mortgage over 30 years.

Borrowers would see the largest dollar amount slashed from their qualification in Greater Vancouver, where the average home price was $1,211,223 in April; they’d receive $47,170 less on their mortgage, and would need to supplement their income by $9,000 to qualify for the same sized mortgage post stress test.

Next was Greater Toronto, where qualification would be reduced by $42,475 on the average home price of $1,090,992, resulting in a requirement of $8,000 in additional income.

The buyers least impacted by the stress test were found in Saskatoon and Winnipeg, where average home prices are $347,616 and $353,377, respectively. Qualification amounts in each would be reduced by $13,661 and $13,875, requiring an income increase of $2,000 to qualify for the same size mortgage.

Check out the infographic below to see how the stress test impacts average home buyers across Canada:

The tougher stress test is part of efforts by both the federal banking regulator (OSFI) and Department of Finance to reduce the amount of risky mortgage debt currently held by Canadians as a result of the pandemic home buying boom. Part of the issue is the aforementioned historically low mortgage rates; interest rates have been kept at record lows over the past year by the Bank of Canada to protect the economy and keep liquidity in the market. However that’s made it cheaper to get a mortgage than ever before; combined with lockdown buyer psychology and pent-up savings, buyers have been motivated to get into the housing market at an unprecedented rate.

That has pushed home prices to stratospheric new heights in markets across Canada, as buyers working and schooling from home have sought properties with more space. The ability to work from home has also decoupled them from big city centres and shifted demand to smaller suburban and rural markets, known for their comparable affordability. However, supply has struggled to keep up with demand. Bidding wars and homes selling for far over their listing price has become the norm, even in secondary markets where these dynamics were previously rare. The Canadian Real Estate Association reports the average home price soared by 41.9% in April to $696,000, with average home prices easily topping the million-mark in the most in-demand markets.

As a result, more home buyers have had to bid higher than they otherwise would have to win their homes, and have taken on larger mortgages. The concern is that when interest rates do inevitably rise, these newly-minted homeowners will struggle to keep up with their mortgage debt. In fact, overly-leveraged households pose one of the largest risks to the economy, according to the Bank of Canada. In their most recent Financial Systems Review, the central bank states, “The biggest domestic vulnerabilities are those linked to imbalances in the housing market and high household indebtedness. These are not new, but they have intensified because of the unusual circumstances caused by the pandemic.”

The BoC adds that buyer expectations have become “extrapolative”, meaning they believe prices will keep rising, fueling their fear of missing out, and hedging on rapidly growing equity in order to afford homes outside of their budgets. This has led to higher levels of mortgage debt, with more borrowers taking on a higher loan-to-income ratio, leaving them potentially financially exposed. The fear is that should an unexpected financial event shock the economy, it could cause a chain reaction of homeowners defaulting on their mortgages.

“It is important to understand that the recent rapid increases in home prices are not normal. Even without a shock, some of the factors that caused prices to rise fast could reverse later, and that could leave some households with less equity in their homes,” states the BoC.

It remains to be seen whether additional methods to cool the housing market will be rolled out by policy makers as the economy recovers from the pandemic. In the meantime, buyers will need to absorb this new affordability requirement when budgeting for their home purchase.

METHODOLOGY:

Average, not seasonally adjusted home prices for April 2021 were sourced from the Canadian Real Estate Association. (CREA) Calculations assumed a home purchase down payment of 20%, 30-year amortization, and no additional debt, no condo fees, $125 heating costs, and $331 property tax. Calculations were made using ratehub.ca/affordability-calculator.

General Robyn McLean 7 Jun

Stay in-the-know on things that affect our economy and the rebound from Covid 19. Valuable information from Dr. Sherry Cooper, Chief Economist at Dominion Lending.

|

|

|

|

|

|

General Robyn McLean 2 Jun

Great insight on our current economic rebound from Dr. Sherry Cooper, Chief Economist at Dominion Lending.

|

|

|

|

|

|

General Robyn McLean 25 May

Some great insight on market conditions from our friends at First National…and even more reason to get honest & informative advice when looking for mortgage financing!

The Bank says these are not new problems, but they have intensified during the pandemic. Consumer debt has actually dropped in the past year or so, but rising mortgage debt has more than offset that decline. At the end of last year Statistics Canada reported that the household debt-to-income ratio stood at 170.7, or $1.71 of debt for every $1.00 of disposable income.

The housing boom has been supporting the overall economy in the short-term but it is also adding to the vulnerability of the economy and financial system. The BoC is also expressing concerns about the declining quality of mortgage borrowing during the pandemic.

The key concern is that any significant economic shock that leads to loss of employment, a drop in income, or a sharp reduction in home prices would force “overstretched” households to cut other spending in order to make their mortgage payments. That, in turn, would curtail the economy as a whole, and could put significant stress on the financial system.

Just because the central bank says there could be a problem, does not mean there will be a problem. There are a number of market watchers who see the Bank using its annual Financial System Review as a bully pulpit in an effort to talk down overly exuberant market expectations that might lead to trouble.

Other key concerns include cybersecurity, too much reliance on cheap credit and the possibility of a premature withdrawal of pandemic support for businesses.

General Robyn McLean 25 May

Some great summer reno tips from Justin Kirby @ REW.

There are plenty of home renovations you can take on this summer, many of which can increase the value of your property. If your renovation attempts this spring didn’t quite go as planned, or if you’ve been putting them off for longer than you intended, get things started while it’s hot outside and the skies are clear. Here are 10 of the most popular home renovations that you can tackle this summer.

With proper care, a good fence should last roughly 15 years. Unfortunately, in wet climates like Vancouver, you’d be very lucky to hit that number. Wood fences eventually rot and need replacing, and it’s not something you want to be doing in the rain. The summer months are the perfect time to replace your fence.

Alternatively, you could plant cedar trees in front of your fence if greenery is more appealing to you. Cedars can be purchased in all sizes; just keep in mind that the taller they are when you buy them, the more expensive they will be.

Deck additions are easily one of the most popular home renovations in 2021. Outdoor gatherings are one of the few ways friends and family can get together during the pandemic, making having a meeting place like a deck or patio extremely valuable. Deck companies are busy right now, so call early or plan to do the work yourself.

If you already have a deck but would like to update it for the summer, adding a new layer of vinyl is a great way to freshen things up. Replacing rotting wood railings with aluminum or glass railings is another excellent way to improve the look of your deck or patio area (and make things safer as well).

A new roof should last you a minimum of 15 years, though they can hold out for much longer than that if you don’t live below large trees. Wood and asphalt shingles are both widespread, though asphalt will need to be replaced sooner in most cases. When it comes to warning signs, watch for any sagging, moss (which can signal trapped moisture), and any patches of shingles that are buckling. If you notice any of these signs, and it’s been over 15 years since the roof was replaced, it’s time to have a professional come out and take a look.

Starting a bathroom remodel can seem daunting at first, but once you begin you’ll see that small spaces really aren’t too overwhelming. Retiling your bathroom floors and shower, replacing showerheads and toilets, hanging new mirrors, and adding a new vanity can be done relatively quickly and leave you with a beautiful new space. These renovations often pay for themselves, as they’ll increase your home’s value when it comes time to sell your property.

The kitchen can be a considerable job depending on how much you want to take on, but a new backsplash is an excellent place to start if you’re looking for a smaller project. A new backsplash can make a kitchen look fresh, or give it a pop of colour depending on your personal preferences. If you’re matching your backsplash colour with your counters (which is common if you’re doing white on white), try to make sure your counters are a slightly warmer tone than your backsplash. This keeps your backsplash looking very clean. Kitchen renovations, in general, are a great way to increase the value of your home.

Interior painting is always a good idea when it comes time to sell your home, but exterior painting shouldn’t be overlooked. The summer months are the perfect time to update the exterior of your home, and adding a fresh coat of paint, even if it’s the same colour as before, really brightens things up. Adding some new trim colours to the exterior, doing a flat stucco job to make things look more modern, or simply removing old wood panelling can go a long way.

Upgrading your windows will not only make your home more attractive and modern, but it will also save you money in the long run. Replacing your windows is one of the best kinds of renovations – those that will save you money every single month, whether you’re keeping the cold air in during the summer months or the warm air in during the winter months. In addition to saving you money on your heating bill, it will also make you money when it comes time to list your property. Double pane, triple pane, and Low-E windows are precisely the kinds of features that energy-efficient buyers are looking for right now.

You’ll likely need to get a permit to frame in your carport, so be sure to check with your city before you begin this renovation project. It’s become extremely popular to opt for a garage instead of a carport for practical and overall home security reasons.

Look for a garage door with good insulation so that your home stays warm in the colder months. The thicker the door, the better, and with no windows if possible – unless the designer in you needs them!

You’ll be surprised by how much this freshens up your home. Whether it’s replacing those ageing doors in your bedrooms, swapping an old sliding door for a set of beautiful french doors, or replacing your front door with a new exciting design and colour, you’ll enjoy this renovation. For a smaller project, you can update every door handle in your home in just a few hours, and this can also add some charm. Black or brass door handles stand out and make an impression.

If you are going ahead with redoing a deck or framing in a carport, there’s a chance you’ll need to re-stucco or add some siding to your new exterior walls. Siding, in particular, is very low maintenance, and if you opt for fibre cement siding, you’ll be choosing a durable product as well. If your home has stucco, try to find someone to match your current style or pattern. This isn’t an easy task, so be sure to go with a professional with a good track record and plenty of reviews.

These home renovation projects are all extremely popular right now. Don’t be afraid to give home improvement a shot this summer. It’s the perfect time to get started.

General Robyn McLean 17 May

Understanding what’s happening in the real estate market from Dr. Sherry Cooper, Chief Economist at Dominion Lending.

|

|

|

|

|

|

|

|

|

General Robyn McLean 10 May

Some invaluable tips from my friends at DLC.

Buying a home is one of the largest investments you will ever make! In order to make your home hunting experience the best it can be, there are a 5 house hunting mistakes to avoid and be aware of before you start your journey:

One of the most important aspects of buying a home is the mortgage application and approval process. No matter what type of home you are looking for, you will need a mortgage. One of the biggest mistakes when it comes to the home-buying process is NOT getting pre-approved prior to starting your search. Getting pre-approved determines the actual home price you can afford as it requires submission and verification of your financial history to ensure the most accurate budget to fit your needs.

Another mistake that people make when home-hunting is not setting, or following, a pre-determined budget. It can be tempting to start looking at the top of your budget, or even slightly over, but when you consider closing costs and the long-term financial responsibility of home ownership, it is best to avoid maxing yourself out. Getting pre-approved will help determine what you can afford, as well as making an appointment with your mortgage broker to determine your financial situation and the best options for you now, and in the future.

Your mortgage broker and your real estate agent are two of the most important members of your homebuying A-Team! In today’s competitive real estate market, it can be very difficult to acquire property without the help of a realtor. One reason is that realtors can provide access to properties that never even make it to the MLS website! They can also gain access to information about homes that may come onto the market, before a listing is even signed. Most importantly though, a realtor understands the ins-and-outs of the home buying process and can tell you how to be successful in your endeavors to purchase a home by guiding you through the process from the first viewing to having your bid accepted.

While we understand that bad interior design can really affect the perception of the home, you don’t want to be blindsided by it. At the end of the day, aesthetics can always be updated! Giving up the perfect price or location or size for a few aesthetic details (such as paint color, flooring, or even outdated appliances or light fixtures) is one of the biggest mistakes people make! Most homes have incredible bones that only need some minor tweaks to become your perfect space.

What you want and need in a house today, could be very different from what you want and need in a house in the future. It is important to be able to look ahead – are you planning on having children? Are your parents getting older and in need of a retirement space? These are things that are good to take into consideration when buying a new home. Buying a home isn’t a permanent decision as you can always sell your home later on if it doesn’t work for you in the future, but it is almost always easier to plan ahead so you can grow with—and not out of—your home whenever possible.