Some great insight on the increase of the stress-test in Canada from our friends at Zoocasa.

How The New Stress Test Will Impact Home Buyer Affordability Across Canada

As of today, it’ll be a bit tougher for new and renewing mortgage borrowers to qualify for their home loan. A higher threshold for the “stress test” has come into effect, requiring borrowers to prove they can carry their mortgage costs at an interest rate of 5.25% or their contract rate plus 2%, whichever is higher. This is a slight increase from the previous threshold of 4.79%. The stricter criteria applies to both insured mortgage borrowers (those who make a down payment smaller than 20% on their home purchase) and uninsured borrowers, who put down 20% or more.

What Does the Stress Test Do?

Simply put, in order to pass the stress test, borrowers must have healthy-enough incomes and debt servicing ratios to indicate they could pay their mortgage payments at the higher interest rate, regardless of the rate they actually get from their lender. For context, current fixed and variable mortgage rates are as low as 1.7% – 2% for a five-year term, so the stress test will tack on at a minimum 3% or higher. This translates to borrowers qualifying for a smaller mortgage amount.

How Will the Stress Test Impact Home Buyers?

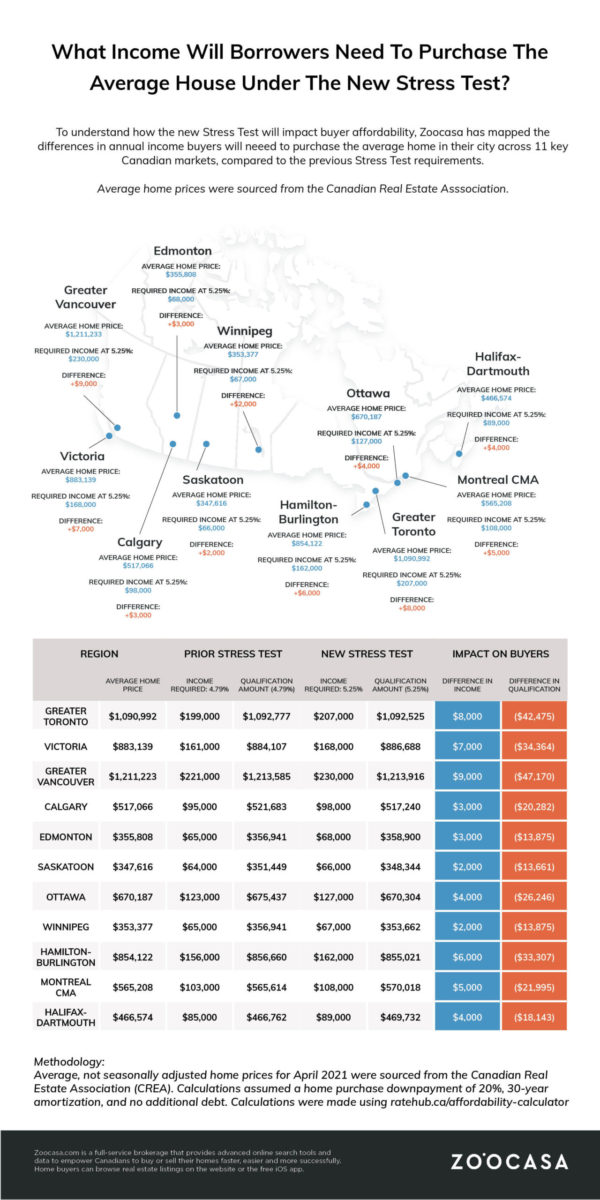

However, as borrowers have been stress tested since 2018, the impact of this latest change will be fairly minimal. According to analysis conducted by Zoocasa, a buyer looking to purchase the average-priced home in their city would face a dip in affordability of about 3.8%, with between $14,000 – $47,000 shaved off the amount they’d qualify for. To make up for this difference, the study determined borrowers would need to supplement their incomes between $2,000 – $9,000 in order to qualify for the same size mortgage under the new stress test, depending on the city they’re purchasing in.

To determine these differences, Zoocasa calculated the income required to qualify for a mortgage large enough to purchase the average-priced home in 11 cities across Canada at both a mortgage rate of 4.79%, and then at 5.25%. It was assumed home buyers had no additional debt, were making a 20% down payment, and were amortizing their mortgage over 30 years.

Borrowers would see the largest dollar amount slashed from their qualification in Greater Vancouver, where the average home price was $1,211,223 in April; they’d receive $47,170 less on their mortgage, and would need to supplement their income by $9,000 to qualify for the same sized mortgage post stress test.

Next was Greater Toronto, where qualification would be reduced by $42,475 on the average home price of $1,090,992, resulting in a requirement of $8,000 in additional income.

The buyers least impacted by the stress test were found in Saskatoon and Winnipeg, where average home prices are $347,616 and $353,377, respectively. Qualification amounts in each would be reduced by $13,661 and $13,875, requiring an income increase of $2,000 to qualify for the same size mortgage.

Check out the infographic below to see how the stress test impacts average home buyers across Canada:

Why Is the Stress Test Being Increased?

The tougher stress test is part of efforts by both the federal banking regulator (OSFI) and Department of Finance to reduce the amount of risky mortgage debt currently held by Canadians as a result of the pandemic home buying boom. Part of the issue is the aforementioned historically low mortgage rates; interest rates have been kept at record lows over the past year by the Bank of Canada to protect the economy and keep liquidity in the market. However that’s made it cheaper to get a mortgage than ever before; combined with lockdown buyer psychology and pent-up savings, buyers have been motivated to get into the housing market at an unprecedented rate.

That has pushed home prices to stratospheric new heights in markets across Canada, as buyers working and schooling from home have sought properties with more space. The ability to work from home has also decoupled them from big city centres and shifted demand to smaller suburban and rural markets, known for their comparable affordability. However, supply has struggled to keep up with demand. Bidding wars and homes selling for far over their listing price has become the norm, even in secondary markets where these dynamics were previously rare. The Canadian Real Estate Association reports the average home price soared by 41.9% in April to $696,000, with average home prices easily topping the million-mark in the most in-demand markets.

As a result, more home buyers have had to bid higher than they otherwise would have to win their homes, and have taken on larger mortgages. The concern is that when interest rates do inevitably rise, these newly-minted homeowners will struggle to keep up with their mortgage debt. In fact, overly-leveraged households pose one of the largest risks to the economy, according to the Bank of Canada. In their most recent Financial Systems Review, the central bank states, “The biggest domestic vulnerabilities are those linked to imbalances in the housing market and high household indebtedness. These are not new, but they have intensified because of the unusual circumstances caused by the pandemic.”

The BoC adds that buyer expectations have become “extrapolative”, meaning they believe prices will keep rising, fueling their fear of missing out, and hedging on rapidly growing equity in order to afford homes outside of their budgets. This has led to higher levels of mortgage debt, with more borrowers taking on a higher loan-to-income ratio, leaving them potentially financially exposed. The fear is that should an unexpected financial event shock the economy, it could cause a chain reaction of homeowners defaulting on their mortgages.

“It is important to understand that the recent rapid increases in home prices are not normal. Even without a shock, some of the factors that caused prices to rise fast could reverse later, and that could leave some households with less equity in their homes,” states the BoC.

It remains to be seen whether additional methods to cool the housing market will be rolled out by policy makers as the economy recovers from the pandemic. In the meantime, buyers will need to absorb this new affordability requirement when budgeting for their home purchase.

METHODOLOGY:

Average, not seasonally adjusted home prices for April 2021 were sourced from the Canadian Real Estate Association. (CREA) Calculations assumed a home purchase down payment of 20%, 30-year amortization, and no additional debt, no condo fees, $125 heating costs, and $331 property tax. Calculations were made using ratehub.ca/affordability-calculator.