Current housing market review by Dominion Lending’s Dr. Sherry Cooper.

The Slowdown In Canadian Housing Continued in May

Today, the Canadian Real Estate Association (CREA) released statistics showing national existing home sales fell 7.4% nationally from April to May 2021, building on the 11% decline in April. Over the same period, the number of newly listed properties fell 6.4%, and the MLS Home Price Index rose 1.0%, a marked deceleration from previous months.

Activity nonetheless remains historically high, but in contrast to March’s all-time record, it is now running closer to levels seen in the second half of 2020 (see chart below). Month-over-month declines in sales activity were observed in close to 80% of all local markets. It was a mixed bag of results, with a slowdown in sales observed in most large markets across Canada.

“While housing markets across Canada remain very active, we now have two months of moderating activity in the books, and that goes for demand, supply and prices,” stated Cliff Stevenson, Chair of CREA. “More and more, there is anecdotal evidence of offer fatigue and frustration among buyers, and the urgency to lock down a place to ride out COVID would also be expected to fade at this point given where we are with the pandemic”.

New Listings

The number of newly listed homes declined by 6.4% in May compared to April. New listings were down in about 70% of all local markets in May.

The national sales-to-new listings ratio was 75.4% in May 2021, down slightly from 76.2% posted in April. The long-term average for the national sales-to-new listings ratio is 54.6%, so it remains historically high; although, it has been moderating since peaking at 90.7% back in January.

Based on a comparison of sales-to-new listings ratio with long-term averages, only about a quarter of all local markets were in balanced market territory in May, measured as being within one standard deviation of their long-term average. The other three-quarters of markets were above long-term norms, in many cases well above.

As the chart below shows, Edmonton was one market in balance, and the Greater Vancouver Area was moving closer to balance, but others remain a seller’s market.

There were 2.1 months of inventory on a national basis at the end of May 2021, up from a record-low 1.7 months in March but still well below the long-term average for this measure of over 5 months.

Home PricesThe Aggregate Composite MLS® Home Price Index (MLS® HPI) rose 1% month-over-month in May 2021 – a noticeable deceleration. The most recent deceleration in month-over-month price growth has come from the single-family space compared to the more affordable townhome and apartment segments.

The non-seasonally adjusted Aggregate Composite MLS® HPI was up 24.4% on a year-over-year basis in May. Based on data back to 2005, this was another record year-over-year increase; although, it is not likely to go much higher.

While the largest year-over-year gains continue to be posted across Ontario, this is also where month-over-month price growth has been slowing the most. Meanwhile, price growth has continued to accelerate in some other parts of the country, thus reducing the year-over-year growth disparity between Ontario and other provinces.

Bottom Line

The near-uniform nature of the housing market activity (in what is usually a highly regionalized market) is still a key feature of this cycle. Indeed, 22 of 26 markets tracked by CREA saw sales fall in May, while all but one market saw the average transaction price up by double-digits from a year ago (sorry, Thunder Bay). Among the tightest markets in the country based on the sales-to-new listings ratio are the Okanagan and Kawartha Lakes; cottage country is still on fire.

The two-month slowdown in Canadian housing is welcome news. The OECD recently released a report showing that New Zealand, Canada and Sweden have the frothiest housing markets in the world. The UK and the US are near the top as well. Clearly, COVID led many around the world to alter their abode, driving prices higher almost everywhere.

Insight on the latest Bank of Canada announcement from our friends at First National.

Jun 9, 2021

First National Financial LP

This morning, in its fourth announcement of 2021, the Bank of Canada left its target overnight benchmark rate unchanged at 0.25%. As a result, the Bank Rate stays at 0.5%. It also provided somewhat encouraging thoughts on the state of, and outlook for, the Canadian and global economies and updated its outlook on inflation. Here is a summary:

Canadian economic conditions

Economic developments have been broadly in line with the Bank’s outlook published in the April Monetary Policy Report

First quarter GDP growth came in at a robust 5.6% and while this was lower than the Bank originally projected, “the underlying details indicate rising confidence and resilient demand”

Household spending was stronger than expected, while businesses drew down inventories and increased imports “more than anticipated”

Economic activity so far in the second quarter has been dampened, largely as anticipated, due to renewed lockdowns associated with the third wave of COVID-19 and recent jobs data show that workers “in contact-sensitive sectors” have once again been negatively affected

Inflation

CPI inflation has risen to around the top of the Bank’s 1-3% inflation-control range, due largely to base-year (2020) effects and much stronger gasoline prices

Core measures of inflation have also risen, due primarily to temporary factors and base year effects, but by much less than CPI inflation

While CPI inflation will likely remain near 3% through the summer, it is expected to ease later in the year, as base-year effects diminish and excess capacity continues to exert downward pressure

Global conditions

With COVID-19 cases falling in many countries and vaccine coverage rising, global economic activity is picking up

The US is experiencing a strong consumer-driven recovery and a rebound is beginning to take shape in Europe, while a resurgence of the virus is hampering the recovery in some emerging market economies

Despite progress on vaccinations, there continues to be uncertainty about the evolution of new COVID-19 variants. However, with provincial containment restrictions on an easing path over the summer, the Bank still expects the Canadian economy to rebound strongly, led by consumer spending. Growth in foreign demand and higher commodity prices should also lead to a solid recovery in exports and business investment, according to the Bank.

With respect to the housing market, the Bank’s only comment was that “activity is expected to moderate but remain elevated.” In April, the Bank opined that housing construction and resales were at historic highs, “driven by the desire for more living space, low mortgage rates, and limited supply” and noted that it would continue to monitor the potential risks associated with the rapid rise in house prices.”

Policy measures

The BoC’s Governing Council noted that there remains considerable excess capacity in the Canadian economy, and that the recovery continues to require “extraordinary monetary policy support.”

Accordingly, the Bank said it remains committed to holding its policy interest rate at what it calls the effective lower bound until economic slack is absorbed and its 2% inflation target is “sustainably achieved.” This may happen sometime in the second half of 2022.

As well, the Bank reiterated that it would continue its Quantitative Easing program – at a target pace of $3 billion per week – to keep interest rates low across the yield curve. It also added that: “Decisions regarding adjustments to the pace of net bond purchases will be guided by Governing Council’s ongoing assessment of the strength and durability of the recovery. We will continue to provide the appropriate degree of monetary policy stimulus to support the recovery and achieve the inflation objective.”

The bottom line

Today’s announcement falls under the heading no news is good news. The benchmark rate is unchanged, the economic recovery appears to be unfolding largely as expected and bond buying activity will continue to provide monetary policy support in the near term.

All of this suggests now is a good time to borrow but also with a view toward developing mid to long-term financing strategies that will address future conditions including the potential for policy interest rate increases next year.

Some great insight on the increase of the stress-test in Canada from our friends at Zoocasa.

How The New Stress Test Will Impact Home Buyer Affordability Across Canada

BY PENELOPE GRAHAM

June 1, 2021

in Infographics, Real Estate News, Toronto Real Estate, Vancouver Real Estate

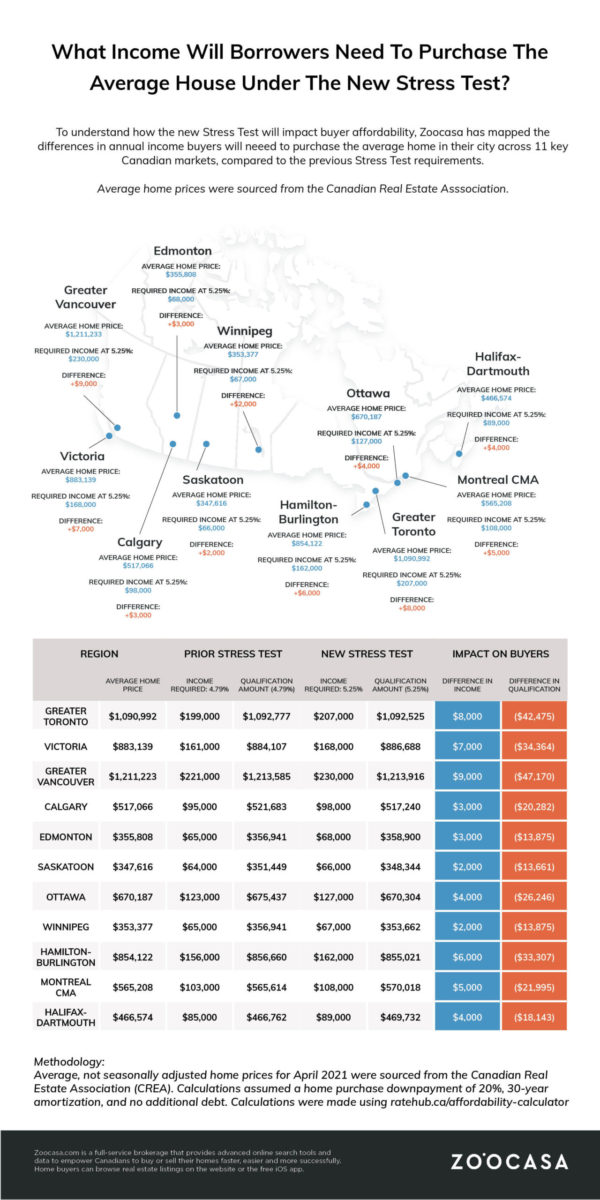

As of today, it’ll be a bit tougher for new and renewing mortgage borrowers to qualify for their home loan. A higher threshold for the “stress test” has come into effect, requiring borrowers to prove they can carry their mortgage costs at an interest rate of 5.25% or their contract rate plus 2%, whichever is higher. This is a slight increase from the previous threshold of 4.79%. The stricter criteria applies to both insured mortgage borrowers (those who make a down payment smaller than 20% on their home purchase) and uninsured borrowers, who put down 20% or more.

What Does the Stress Test Do?

Simply put, in order to pass the stress test, borrowers must have healthy-enough incomes and debt servicing ratios to indicate they could pay their mortgage payments at the higher interest rate, regardless of the rate they actually get from their lender. For context, current fixed and variable mortgage rates are as low as 1.7% – 2% for a five-year term, so the stress test will tack on at a minimum 3% or higher. This translates to borrowers qualifying for a smaller mortgage amount.

How Will the Stress Test Impact Home Buyers?

However, as borrowers have been stress tested since 2018, the impact of this latest change will be fairly minimal. According to analysis conducted by Zoocasa, a buyer looking to purchase the average-priced home in their city would face a dip in affordability of about 3.8%, with between $14,000 – $47,000 shaved off the amount they’d qualify for. To make up for this difference, the study determined borrowers would need to supplement their incomes between $2,000 – $9,000 in order to qualify for the same size mortgage under the new stress test, depending on the city they’re purchasing in.

To determine these differences, Zoocasa calculated the income required to qualify for a mortgage large enough to purchase the average-priced home in 11 cities across Canada at both a mortgage rate of 4.79%, and then at 5.25%. It was assumed home buyers had no additional debt, were making a 20% down payment, and were amortizing their mortgage over 30 years.

Borrowers would see the largest dollar amount slashed from their qualification in Greater Vancouver, where the average home price was $1,211,223 in April; they’d receive $47,170 less on their mortgage, and would need to supplement their income by $9,000 to qualify for the same sized mortgage post stress test.

Next was Greater Toronto, where qualification would be reduced by $42,475 on the average home price of $1,090,992, resulting in a requirement of $8,000 in additional income.

The buyers least impacted by the stress test were found in Saskatoon and Winnipeg, where average home prices are $347,616 and $353,377, respectively. Qualification amounts in each would be reduced by $13,661 and $13,875, requiring an income increase of $2,000 to qualify for the same size mortgage.

Check out the infographic below to see how the stress test impacts average home buyers across Canada:

Why Is the Stress Test Being Increased?

The tougher stress test is part of efforts by both the federal banking regulator (OSFI) and Department of Finance to reduce the amount of risky mortgage debt currently held by Canadians as a result of the pandemic home buying boom. Part of the issue is the aforementioned historically low mortgage rates; interest rates have been kept at record lows over the past year by the Bank of Canada to protect the economy and keep liquidity in the market. However that’s made it cheaper to get a mortgage than ever before; combined with lockdown buyer psychology and pent-up savings, buyers have been motivated to get into the housing market at an unprecedented rate.

That has pushed home prices to stratospheric new heights in markets across Canada, as buyers working and schooling from home have sought properties with more space. The ability to work from home has also decoupled them from big city centres and shifted demand to smaller suburban and rural markets, known for their comparable affordability. However, supply has struggled to keep up with demand. Bidding wars and homes selling for far over their listing price has become the norm, even in secondary markets where these dynamics were previously rare. The Canadian Real Estate Association reports the average home price soared by 41.9% in April to $696,000, with average home prices easily topping the million-mark in the most in-demand markets.

As a result, more home buyers have had to bid higher than they otherwise would have to win their homes, and have taken on larger mortgages. The concern is that when interest rates do inevitably rise, these newly-minted homeowners will struggle to keep up with their mortgage debt. In fact, overly-leveraged households pose one of the largest risks to the economy, according to the Bank of Canada. In their most recent Financial Systems Review, the central bank states, “The biggest domestic vulnerabilities are those linked to imbalances in the housing market and high household indebtedness. These are not new, but they have intensified because of the unusual circumstances caused by the pandemic.”

The BoC adds that buyer expectations have become “extrapolative”, meaning they believe prices will keep rising, fueling their fear of missing out, and hedging on rapidly growing equity in order to afford homes outside of their budgets. This has led to higher levels of mortgage debt, with more borrowers taking on a higher loan-to-income ratio, leaving them potentially financially exposed. The fear is that should an unexpected financial event shock the economy, it could cause a chain reaction of homeowners defaulting on their mortgages.

“It is important to understand that the recent rapid increases in home prices are not normal. Even without a shock, some of the factors that caused prices to rise fast could reverse later, and that could leave some households with less equity in their homes,” states the BoC.

It remains to be seen whether additional methods to cool the housing market will be rolled out by policy makers as the economy recovers from the pandemic. In the meantime, buyers will need to absorb this new affordability requirement when budgeting for their home purchase.

METHODOLOGY:

Average, not seasonally adjusted home prices for April 2021 were sourced from the Canadian Real Estate Association. (CREA) Calculations assumed a home purchase down payment of 20%, 30-year amortization, and no additional debt, no condo fees, $125 heating costs, and $331 property tax. Calculations were made using ratehub.ca/affordability-calculator.

Stay in-the-know on things that affect our economy and the rebound from Covid 19. Valuable information from Dr. Sherry Cooper, Chief Economist at Dominion Lending.

Canada’s Jobs Recovery Derailed By Third-Wave Restriction

This morning, Statistics Canada released the May 2021 Labour Force Survey showing another contraction in employment, albeit not as dramatic as in April. With the geographical broadening in lockdown restrictions in May, employment fell by 68,000 (-0.4%), but almost all of the decline was in part-time work. The number of self-employed workers was virtually unchanged in May but remained 5.0% (-144,000) below its pre-pandemic level.

Among people working part-time in May, almost one-quarter (22.7%) wanted a full-time job, up from 18.5% in February 2020 (not seasonally adjusted).

The number of Canadians working from home held steady at 5.1 million. This is similar to the number of telecommuters in the spring of last year.

After falling in April, total hours worked were little changed in May.

Employment in the goods-producing sector dropped for the first time since April 2020, with decreases in both the manufacturing and construction industries. Ontario and Nova Scotia were the only provinces to register declines in total employment.

Employment increased in Saskatchewan, while there was little change in all other provinces.

Unemployment little changed

The unemployment rate was little changed at 8.2% in May, as the number of people who searched for a job or who were on temporary layoff held steady. The unemployment rate remained lower than the recent peak of 9.4% seen in January 2021 and considerably lower than its peak of 13.7% in May 2020.

The unemployment rate among visible minority Canadians aged 15 to 69 rose 1.5 percentage points to 11.4% in May (not seasonally adjusted).

Long-term unemployment—the number of people unemployed for 27 weeks or more—held relatively steady at 478,000 in May.

Full-time employment was little changed in May, following a decline of 129,000 (-0.8%) in April. Before April, full-time employment had steadily trended upwards, following the low in April 2020. In May 2021, the number of full-time workers was down 1.9% (-303,000) from its pre-pandemic level.

Private sector employees in sales and services most affected by restrictions

The number of private-sector employees declined by 60,000 in May (-0.5%), adding to losses observed in April (-204,000; -1.7%). This followed employment gains totalling 427,000 in February and March 2021—demonstrating the extent to which employment for this group of workers has been affected by the easing and tightening public health measures introduced to contain the COVID-19 pandemic.

Compared with February 2020, the number of private-sector employees was down 564,000 (-4.6%), with the gap driven mostly by declines in the number of people working in the accommodation and food services industry, particularly those working in sales and services occupations (not seasonally adjusted).

Employment in construction falls with tightening of public health restrictions in ON

Employment in construction fell by 16,000 (-1.1%) in May, driven by declines in Ontario, where public health restrictions affecting non-essential construction were implemented on April 17. The decrease brought the number of workers in construction down to 3.7% (-55,000) below pre-COVID levels.

Bottom Line

With the easing of COVID restrictions beginning this month, we expect a sharp bounceback in job creation starting in the next employment report. The potential for a sharp rebound and a faster-than-expected full recovery has already prompted the Bank of Canada to start tapering its stimulus with reduced bond buying. Markets are expecting rate hikes by the Bank to begin next year.

Canada’s economy remains 571,100 jobs shy of pre-pandemic levels. The unemployment rate was below 6% before the pandemic.

The Canadian jobs report coincided with the release of U.S. payroll numbers, which increased by 559,000 last month — short of an expected 675,000–but well above the surprisingly weak job growth in April.

Great insight on our current economic rebound from Dr. Sherry Cooper, Chief Economist at Dominion Lending.

Housing Drove the Economic Expansion in Q1

Yesterday’s Stats Canada release showed that the economy grew at a 5.6% annualized rate in the first quarter, after a revised 9.3% pace in the final quarter of last year. That was somewhat below economists’ expectations. Housing investment grew at an annualized 43% pace, by far the biggest impetus of the expansion. Residential investment now makes up a record proportion of GDP (see chart below). Compared with the first quarter of 2020, housing investment was up 26.5% and led the recovery. Growth in housing was attributable to an improved job market, higher compensation of employees, and low mortgage rates. After adding $63.6 billion of residential mortgage debt in the last half of 2020, households added $29.6 billion more in the first quarter of 2021.

Residential investment is a component of the Gross Domestic Product accounts and is technically called ‘gross fixed capital formation in residential structures’ by Statistics Canada. Investment in residential structures is comprised of three components: 1) new construction, 2) renovations and 3) ownership transfer costs. The first two components are obvious.

The home-resale market’s contribution to economic activity is reflected in ‘ownership transfer costs.’ These costs are as follows:

real estate commissions–including realtors and mortgage brokerage fees;

land transfer taxes;

legal costs (fees paid to notaries, surveyors, experts etc.); and

file review costs (inspection and surveying).

The second chart below shows the quarterly percent change in the components of housing investment in inflation-adjusted terms. This chart illustrates the surge in existing home sales since the second quarter of last year (reflected in the red bar). Although the resale market has slowed since the third quarter of last year, it remains a driving force of economic expansion.

Growth in housing investment was broad-based. New construction rose 8.7% (quarter-over-quarter), largely driven by detached units in Ontario and Quebec. Ownership transfer costs increased 13.1%, with the rise in resale activities. Working from home and extra savings from reduced travel heightened the demand for, and scope of, home renovations, which grew 7.0% in the first quarter.

The increase in GDP in the first quarter of 2021 reflected the continued strength of the economy, influenced by favourable mortgage rates, continued government transfers to households and businesses, and an improved labour market. These factors boosted the demand for housing investment while rising input costs heightened construction costs.The GDP implicit price index, which reflects the overall price of domestically produced goods and services, rose 2.9% in the first quarter, driven by higher prices for construction materials and energy used in Canada and exported. The sharp increase in prices boosted nominal GDP (+4.3%). Compensation of employees rose 2.1%, led by construction and information and cultural industries, and surpassed the pre-pandemic level recorded at the end of 2019.

Strength in oil and gas extraction, manufacturing of petroleum products, and construction industries led to a higher gross operating surplus for non-financial corporations (+11.5%). Higher earnings from commissions and fees bolstered the operating surplus of financial corporations (+3.9%), coinciding with the sizeable increases in the value and volume of stocks traded on the Toronto Stock Exchange (TSX).

Most aspects of final sales were solid in Q1, with consumers a bit stronger than expected (2.8% a.r.), government adding (5.8%), and net exports also contributing. In contrast, business investment was one real source of disappointment, with equipment spending surprisingly falling. But the biggest drag came from a drop in inventories, with this factor alone cutting growth 1.4 ppts in Q1, and versus expectations, it could add a touch. The good news is that this should reverse in Q2, supporting activity in the current quarter.

On the monthly figures, there were few big surprises. March’s initial flash estimate of +0.9% was nudged up in the official estimate to +1.1% as the economy began to re-open from the second wave. Tougher COVID public health rules slammed the brakes on Canada’s economy in April. Statistics Canada estimates gross domestic product shrank 0.8% in the month, representing the first contraction in a year and a weak handoff heading into the second quarter. April may well be followed by a soft May. Even so, we still expect a strong June will keep Q2 roughly flat overall and look for robust Q3 growth.

Bottom Line

In many respects, Q1 data is ancient history. We know with the resurgence in lockdowns, growth in Q3 will at best be flat. In the hopes that vaccinations will accelerate and COVID case numbers will continue to fall across the country, Q4 will likely see a strong resurgence in growth.