Valuable insight aimed at helping us all to understand more as we navigate through this difficult time from DLC’s Chief economist, Dr. Sherry Cooper

|

General Robyn McLean 30 Mar

Valuable insight aimed at helping us all to understand more as we navigate through this difficult time from DLC’s Chief economist, Dr. Sherry Cooper

|

General Robyn McLean 27 Mar

From DLC’s Chief Economist, Dr. Sherry Cooper. Important steps towards our financial recovery!

|

|

|

General Robyn McLean 27 Mar

The last two weeks have ushered in a time of financial and public health uncertainty that’s unprecedented for many Canadians. As governments enact measures to keep the public safe from COVID-19 community spread, with the closing of schools, small businesses, and other non-essential services, many are questioning what the economic impact will be for all, from individuals to entire industries.

While we all do our part to “flatten the curve” by working remotely if possible, avoiding gathering in public, and going out only on a need-to basis, businesses that require an in-person approach are having to make drastic changes to continue to operate – and that includes the real estate industry.

The home buying and selling process typically requires a personal connection between real estate agents and their clients; from the first in-person meeting to discuss their needs, to the viewing of open houses and delivery of deposit funds, real estate transactions are typically hands on.

However, while real estate brokerages and agent services have been considered “essential services” in some provinces including Ontario, the strong recommendation from municipal and provincial real estate bodies is to stop operations altogether in order to comply with best social distancing practices. This comes after a call last week to cancel all open houses, and make all showings virtual, to be conducted on an only as-needed basis. As well, it has been strongly discouraged to show homes that are currently tenanted.

The bottom line is, as long as these health risks are present, it’s widely expected that anyone without an urgent need to buy or sell a home will put their real estate ambitions on hold for the time being. That bodes a lot of questions for the market in general; what will be the immediate impact? When the threat of COVID-19 dissipates, will prospective home buyers still be there to pick the market back up?

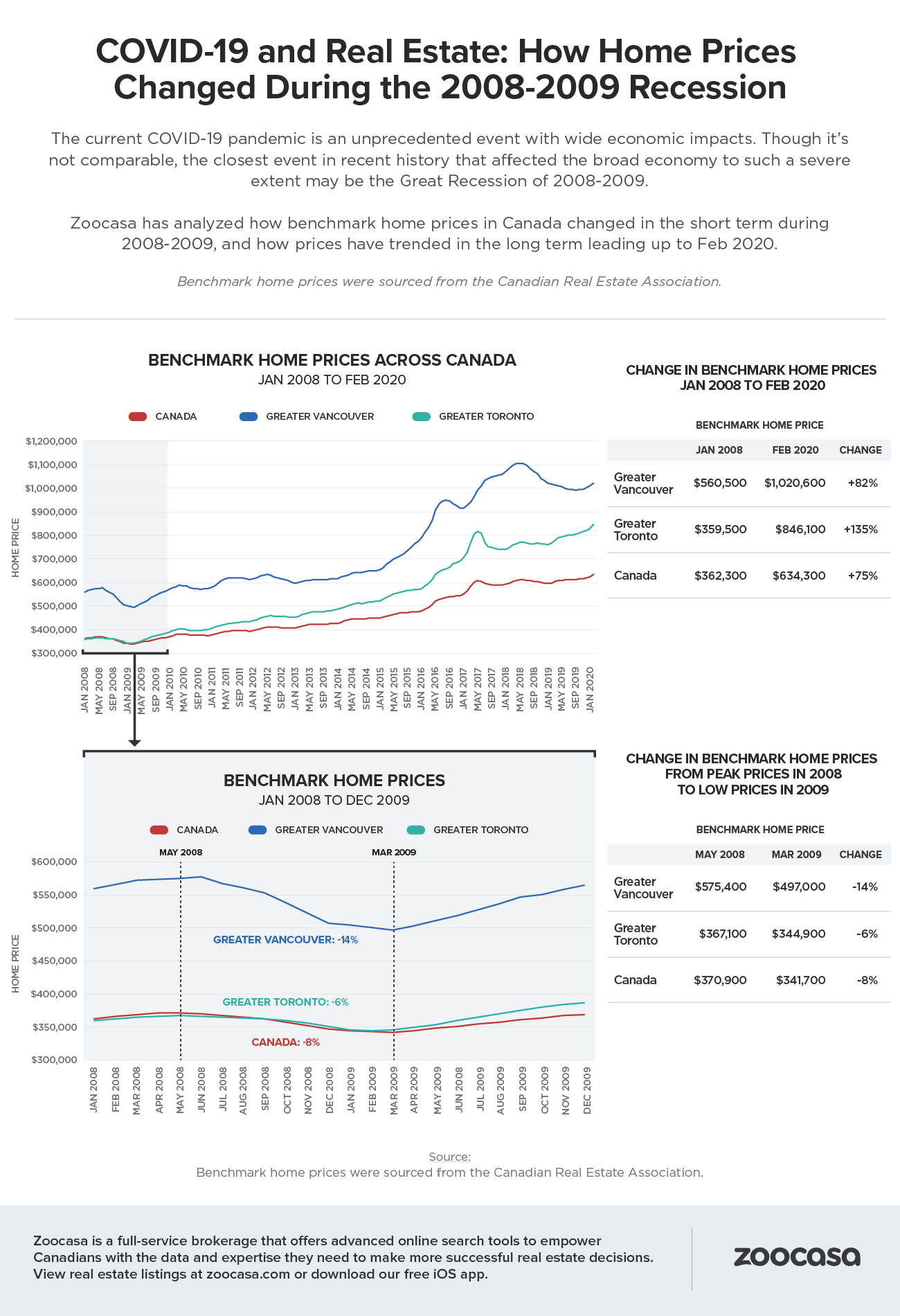

To get an idea of how COVID-19 could shape the housing market in the short- and long-term, let’s take a look at a similar scenario that led to slower market conditions.

Though the circumstances are very different, the closest economic event that’s comparable to the impact of COVID-19 is the 2008 – 2009 global recession, which was spurred by mass defaults in mortgage debt and resulted in similar monetary policy moves from central banks to mitigate the damage, along with bank bailouts and stock market upheaval. While Canada has been lauded for fiscally weathering that recession better than many nations, home prices did see a drop during its deepest crevice, between the springs of 2008 and 2009.

According to analysis by Zoocasa, benchmark real estate prices dipped across the nation during this time period by -8%, from $370,900 to $341,700. The drop was most pronounced in the Greater Vancouver real estate market, which experienced a -14% decline, from $575,400 to $497,000. Losses remained under double-digit percentages for Toronto homes for sale, down -6% from $367,100 to $344,900.

However, as anyone who has been witness to the Canadian housing market over the last decade can attest, these losses were largely contained to the period of economic downturn, with enormous growth seen between January 2008 – February 2020. Canada-wide, home values have surged 75%, from $362,300 to $634,300, while gains were even more pronounced in the largest urban centres. Vancouver home prices rose 82% from $560,500 to today’s searing price tag of $1,020,600, while Toronto home prices were up a whopping 135% from $359,500 to $846,100.

While it’s impossible to predict just how long COVID-19 will impact the economy, Lauren Haw, Zoocasa’s CEO and Broker of Record, points out that the fundamentals of the housing market, especially in large cities such as Toronto and Vancouver, generally don’t change. “There has long been a lot of pent-up buyer demand in these markets, particularly due to a long-term lack of inventory,” she says. “Combined with continued population growth in these regions, it’s expected that the market will experience a strong bounce back once the health risks have subsided, and buyers return to the market with restored purchasing power.”

General Robyn McLean 26 Mar

Some valuable information if you’re a renter right now struggling to pay your rent due to the Covid-19 pandemic.

If you are renting in Canada currently, you may be facing some uncertainties about your future amid the COVID-19 pandemic – especially with the start of a new month on the horizon. Provincial governments are currently rolling out plans to help renters during this time:

British Columbia: The B.C. government has imposed a moratorium on residential evictions. In addition, they will be providing renters with up to $500 per month for the next four months to help you manage your rent payments. Premier John Horgan also announced a provincial freeze on rental increases during this time.

Alberta: Alberta currently is considering a short term stay on eviction enforcement but no plan has been made as of yet.

Manitoba: Manitoba Premier Brian Pallister has postponed all hearings for non-urgent matters to avoid evictions resulting from non-payment of rent. In addition, any rent increases scheduled to take effect on April 1 or later are being suspended.

Saskatchewan: No COVID-19 rental policies currently in place.

Ontario: Ontario has suspended eviction orders resulting from non-payment of rent until further notice. Further, plans are in development.

Quebec: Has suspended most eviction hearings amid COVID-19.

Nova Scotia: Has banned evictions resulting from non-payment of rent.

Prince Edward Island: Has banned evictions resulting from non-payment of rent.

Northwest Territories: Has banned evictions resulting from non-payment of rent.

| ADDITIONAL FINANCIAL MEASURES |

In addition to helping homeowners manage their finances through deferred mortgage payments and adjustments, the Canadian Government has also come to the aid of families who may be struggling currently.

To help those currently struggling, the following measures are being taken or have already been implemented:

In addition, the Canada Revenue Agency is adapting their Outreach Program in order to better support individuals during COVID-19. This service allows the CRA to offer assistance to ensure individuals understand their tax obligations and to help them obtain the benefits and credits to which they are entitled.

General Robyn McLean 19 Mar

At Dominion Lending Centres, we are deeply concerned about the Coronavirus – and we know you are too. Our thoughts and prayers go out to all the families and front line workers that are dealing with this around the world.

We recognize that many homeowners may be looking for guidance around mortgage financing. We are committed to updating you – our customers – on the current climate and how the recent COVID-19 developments may impact your mortgage, now or in the future. We know that things may seem uncertain now, but we are working hard to gather all pertinent information and help you to understand your options during this difficult time.

As many of you have heard by now, the world is being gripped by COVID-19 (otherwise known as “Coronavirus”). According to the World Health Organization (W.H.O.), Coronaviruses (CoV) is a large family of viruses ranging from the common cold to more severe diseases.

Coronavirus disease (COVID-19) is a new strain that was discovered in 2019 and has not been previously identified in humans. Common signs of infection include respiratory symptoms, fever, cough, shortness of breath and breathing difficulties. In more severe cases, infection can cause pneumonia, severe acute respiratory syndrome, kidney failure and even death.

Standard recommendations to prevent infection spread include regular hand washing, covering mouth and nose when coughing and sneezing, thoroughly cooking meat and eggs. Avoid close contact with anyone showing symptoms of respiratory illness such as coughing and sneezing.

| UPDATE 1: | FINANCIAL EFFECTS |

Since being labeled a pandemic per the World Health Organization (W.H.O.), the effects of COVID-19 have begun to ripple through the world’s economy – including Canada – and causing a number of different effects. To help keep you up to date on what is going on financially, we have compiled a list of recent announcements by the Ministry of Finance, the Bank of Canada, and OSFI:

In addition, Dominion Lending Centres in-house Chief Economic Advisor, Dr. Sherry Cooper, has been providing in-depth information on this situation as it evolves. You can find her latest articles on the situation below:

| UPDATE 2: | HOMEOWNER NEED TO KNOW |

This can be a difficult time for a homeowner as many families are self-isolating or are in quarantine due to the virus. This can result in loss of monthly income and financial instability, which can cause stress and concern about your home and mortgage. Dominion Lending Centres understands this and we are making it our number one priority to be here for you.

We have compiled the following information from our partners to keep you informed as to some of the recent developments surrounding mortgages, as well as what lenders are doing to help mitigate financial strain during this difficult time.

Here are a few important considerations for homeowners and potential homeowners to keep in mind during this time:

In lieu of this growing situation, OSFI has announced that it is suspending all consultations, including those regarding changes to the proposed B-20 benchmark rate. In addition, the Minister of Finance postponed the announced April 6th qualification change for insured mortgages. In short, until further notice, the Bank of Canada posted a 5-year rate will continue to be used for mortgage qualification.

| UPDATE 3: | WHAT LENDERS ARE DOING |

We understand that the COVID-19 outbreak is taking a toll on families across the country with many parents being out of work or quarantined. As an industry built on homeowners, many of our major lenders have pulled together to provide you beneficial options during this time and help alleviate some of the financial stress.

Depending on your lender, there may be options available to you during this time such as:

Big banks including Royal Bank of Canada (RBC), Toronto-Dominion Bank (TD), Bank of Nova Scotia (Scotiabank), Bank of Montreal (BMO), Canadian Imperial Bank of Commerce (CIBC) and National Bank of Canada have opted to provide coordinated relief for their customers.

These banks will be working with personal and small business clients to cope with the economic fallout of the virus. Effective immediately, all six are introducing mortgage payment deferrals of up to (6) months and are also offering relief on other credit products for those families who are facing hardship during this situation.

In addition to the big banks, mortgage insurers including CMHC, Genworth & Canada Guaranty are working to help homeowners who have been financially impacted by the COVID-19 outbreak. Starting now, they have increased their flexibility and are allowing payment deferral of up to 6 months for home-owners who, primarily but not exclusively, purchased with less than 20% down.

Genworth Canada released a statement on March 16, 2020 outlining their Homeowner Assistance Program (HOAP), which is designed to assist Genworth Canada-insured homeowners who experience sudden financial setbacks that could temporarily impact their ability to meet their mortgage obligations. Borrowers who qualify under the lender’s internal guidelines and Genworth’s Homeowner Assistance Program will receive up to six (6) months of relief allowing borrowers some time to recover and focus on what’s important.

Canadian Mortgage and Housing Corporation (CMHC) is offering tools that can assist homeowners who may be experiencing financial difficulty. Their default management tools include: payment deferral, loan re-amortization, capitalization of outstanding interest arrears and other eligible expenses and special payment arrangements.

CMHC also provides mortgage professionals with tools and the flexibility to make timely decisions when working with you to find a solution to your unique financial situation, including:

In addition to Genworth Canada and CMHC, Canada Guaranty is also doing their part to support homeowners during this difficult time. Per their statement released on March 16, 2020 they noted with their Homeownership Solutions Program, lenders currently have the ability to capitalize up to four (4) monthly mortgage payments.

However, to assist eligible homeowners as they navigate through these challenging circumstances, Canada Guaranty is prepared to extend this program option to allow the capitalization of up to a maximum of six (6) monthly payments. This is assuming the original insured loan amount is not exceeded, request for capitalization is received before September 13, 2020 and that the lender confirms the capitalization is being applied reasonably to help mitigate short-term financial difficulty resulting from COVID-19.

During this time, it is best to discuss your mortgage with your mortgage broker or lender should you have any financial concerns surrounding the COVID-19 outbreak. Please be advised, there may be longer than normal wait times for calls during this situation and to expect at least 20-30 minutes for a representative. Be sure to have your mortgage number available to ensure smoother service and remember to be kind!

Here are some direct contact numbers for various lenders across the country:

| LENDERS | CONTACT # |

|---|---|

| ATB | 1-800-332-8383 |

| B2B | 1-800-263-8349 |

| Bank of Montreal | 1-877-895-3278 |

| Bridgewater | 1-866-243-4301 |

| Chinook Financial | 403-934-3358 |

| CIBC | 1-800-465-2422 |

| CMLS Financial | 1-888-995-2657 |

| Connect First | 403-520-8000 |

| Equitable | 1-866-407-0004 |

| First Calgary Financial | 403-736-4000 |

| First National | 1-888-488-0794 |

| Haventree | 1-855-727-0051 |

| Home Trust | 1-855-270-3630 |

| HomeEquity Bank | 1-866-331-2447 |

| HSBC | 1-888-310-4722 |

| ICICI | 1-888-424-2422 |

| Manulife | 1-800-268-6195 |

| Marathon | 1-855-503-6060 |

| MCAP | 1-866-809-5800 |

| Merix | 1-877-637-4911 |

| National Bank | 1-888-835-6281 |

| Optimum | 1-866-441-3775 |

| RFA | 1-877-416-7873 |

| RMG | 1-866-809-5800 |

| Royal Bank | 1-800-768-2511 |

| Scotiabank | 1-800-472-6842 |

| Servus | 1-877-378-8728 |

| Street Capital | 1-866-683-8090 |

| TD | 1-888-720-0075 |

| UPDATE 4: | WHAT DOES THIS MEAN FOR CLOSINGS? |

If you are currently in the process of purchasing or selling a home, we have taken the liberty of gathering information surrounding real estate transactions during this COVID-19 situation.

Currently, there are no plans to close the LROs. This may change, but currently, LROs may be working with reduced staff and will likely prioritize services required for closings (over-rides, pre-approvals, PIN corrections, etc.)

All of Canada’s major banks have indicated an intention to remain open. Similar to other businesses, the banks may be working with reduced staff or locations and there may be delays in processing requests.

Tarion

Tarion issued an Advisory on Friday confirming that the builder repair period has been suspended until April 13, 2020, and that homeowners may refuse access and builders may refuse to perform after-sales services during the COVID-19 pandemic without penalty.

Client Meetings

Due to the focus on self-isolation and preventing further spread of COVID-19, there may be issues with clients not being able to meet with lawyers/notaries – or vice versa. Remote meetings are still a great option during this time (both in real estate and for your mortgage professional) and can be held via phone or video conference with a plan to provide any sworn documents at a later date. If you do meet in-person, don’t shake hands, sit as far apart as possible and be sure to wash your hands after leaving any unfamiliar environments.

Municipalities

There have been recommendations that people limit in-person interactions, work from home if possible and not go out for ‘non-essential’ reasons. It is now very possible that municipalities may close their offices or work with reduced staff and that delays in receiving compliance information, permits and municipal agreements may be experienced.

If either the LRO or the banks close, then real estate transactions will not be able to proceed and you would need to seek extensions wherever possible. The good news is that everyone is in the same situation! The bad news is that there is no right in most re-sale agreements to insist on an extension, however, most people are understanding and you will have to rely on their goodness as well as common law principles to extend the transaction.

| UPDATE 5: | WHAT CAN YOU DO? |

If you find yourself facing financial difficulties as a result of job loss or income reduction during this time, it can be overwhelming and may leave you feeling stressed and unsure of what the next steps are.

To make it easy, we have put together three simple steps you can do to help resolve your financial difficulties and ensure you can focus on more important things such as your family and your health.

| UPDATE 6: | STAY SAFE – AND WASH YOUR HANDS! |

Remember during this time to practice proper hand-washing procedures and minimize your contact with other people to ensure that you are not unknowingly contracting or passing along COVID-19. We can overcome this, together.

General Robyn McLean 17 Mar

Information is power, particulary in such tumultuous times. DLC’s Chief Economist Dr. Sherry Cooper offers her insights.

|

|

|

|

|

|

|

|

|

|

|

|

General Robyn McLean 15 Mar

Some good tips on keeping your family safe at home from our friends at REW.

COVID-19 or the Coronavirus is undoubtedly challenging to ignore. It is the topic of conversation with every social encounter, and it is the leading news story on all the stations. It is washing over our newsfeeds every few seconds. With all the hype and talk of the pandemic, now more than ever, stay calm and, well, clean.

We’ve heard the best defence against COVID-19 is hand washing. While that is true, there are other things you can be doing on the home front to battle this beast. Let’s take a look at some of the top measures.

The spread of COVID-19 is primarily from invisible respiratory droplets that fly through the air when a sick person coughs or sneezes. Others inhale these droplets, and they land on surfaces. When a person touches the surface, they become infected when they feel their eyes, nose, or mouth.

It would only make sense to clean the surfaces in our home to ensure maximum defence against the virus. But, will your favourite go-to cleaner do the trick?

Studies show common household disinfectants, including soap or diluted bleach solutions, can deactivate coronaviruses on indoor surfaces.

The Centre for Disease Control (CDC) recommends using a mixture of bleach and water to disinfect floors. They suggest 1 cup of bleach mixed with 5 gallons of water to mop your floors is the most effective. Although this is one way to go, be careful when using bleach to disinfect.

Studies have shown that bleach is highly irritating to mucous membranes. People exposed to bleach fumes are at risk of respiratory troubles, among other ailments. So, although it works, use it sparingly.

If you are looking for something a little less harsh – and very affordable, vinegar may be an option. It is an all-natural disinfectant that contains acetic acid. Choose plain old white distilled vinegar. And while you are at it, you can use a vinegar spray on your fruits and vegetables to help kill germs and wash away potential pesticides.

It’s perfect for doorknobs, mirrors, porcelain, and most surfaces.

Hydrogen Peroxide is not just for treating cuts and scrapes. It can also be used as a general household cleaner too. Make sure you store it in a dark container away from sunlight as the light will destroy its beneficial properties. The CDC reports that 3% hydrogen peroxide was able to inactivate rhinovirus within eight minutes. When you pour the substance directly on surfaces like your sink, countertops or toilets, you’ll need to let it soak for around 10-15 minutes to give it time to do its job completely. After you let it sit, scrub the area and then rinse with water.

Don’t forget about the germs on your toothbrush! You can use hydrogen peroxide to keep it fresh.

Seriously. Ten years ago, people barely heard of essential oils. Now they are being used to treat a variety of ailments. Tea Tree Oil is versatile and can e used in a variety of situations. It is also known as Melaleuca Oil is one of the best natural alternatives to harsh cleaners. www.cdc.gov/disasters/bleach.html it’s a great household cleaner when mixed with water. Because it’s extremely concentrated, all you need is a few drops mixed with water to create an effective disinfectant. Mix it in a spray bottle and use on countertops, tile, door handles, sinks, toilets. It is even effective on soft surfaces.

Bonus Tip: tea tree oil is excellent for making your own hand sanitizer, disinfecting areas where pets may have had an accident or where kids may have gotten sick. There is no end to where you can use this natural powerhouse.

In a hurry? Use disinfectant wipes to go over surfaces quickly. Phones, doorknobs, sinks, cabinet handles, refrigerator doors, remote controls – the surfaces you touch most often in your home are a magnet for germs. Wipe down a couple of times a day. For the best results, let the surface air dry to kill any lingering bacteria or viruses. Tip: Don’t have any wipes? Make your own by spraying a paper towel with a tea tree oil mixture.

For soft surfaces like sofas and carpets, a disinfectant spray will do the trick (most stores and pharmacies carry 70% alcohol spray). It would also work on mattresses, countertops or tables. A broad sweeping spray works best. Let dry before you walk, sit, or use the surface.

For more safe product information, the Environmental Protection Agency has a list of disinfectants that have shown to be effective in fighting coronaviruses.

And remember, during these uncertain times, remain calm and clean.

General Robyn McLean 10 Mar

Planning to sell? Here’s a valuable tip from our friends at Pillar to Post.

A pre-listing home inspection can uncover previously unknown problems – major and minor – allowing your sellers the opportunity to make repairs, updates or replacements as needed or as they wish.

By addressing issues before the home goes on the market, you can list a home with greater confidence about its condition. This can mean cleaner offers and a smoother transaction for both parties. And a home in better condition will normally sell for more than one with problems that could have been corrected.

Homes that are already on the market can be at a disadvantage if problems are revealed during a subsequent home inspection. Issues that you and the seller were previously unaware of could keep a property from selling at its highest potential price, when it’s too late to address them.

The Pillar To Post Home Inspection includes a comprehensive report, complete with photos, printed on-site so there’s no waiting for results. With this valuable information in hand, your sellers can decide on next steps prior to listing. In the end, having well-informed sellers and buyers will work to everyone’s advantage, including yours.

General Robyn McLean 9 Mar

Insight on today’s enormous market drop from DLC’s Chief Economist, Dr. Sherry Cooper.

Markets shuddered in the face of a price war for oil and the economic fallout from the growing outbreak of coronavirus. Frightened investors poured into haven assets sending yields to unprecedented lows. Oil prices tumbled 30% after Saudi Arabia said it would cut most of its oil prices and boost output when Russia refused to join OPEC in propping up prices (see chart below). Foreign exchange markets convulsed, as the steep drops in oil and share prices overnight sparked a flight from commodity-linked currencies into the perceived safety of the Japanese yen and the US dollar. The Canadian dollar fell to 0.7362 as of this writing. The Government of Canada 5-year bond yield was as low as 0.284% overnight but has since recovered roughly 0.535%, still well below Friday’s closing level of approximately 0.65% (second chart below).

Stock prices have fallen very sharply in the first hour of North American trading. Panic selling sent the Dow down 2,000 points, and the S&P500 sank 7% after triggering a circuit breaker that halted trade for 15 minutes. The TSX took a dizzying nosedive on the open, down more than 1400 points or nearly 9.0% led down by oil stocks and financials.

The spread of coronavirus outside of China tripled over the past week. The US State Department announced yesterday that older people should avoid travel on cruises, particularly if they have compromised immune systems. All of this amplifies recession fears as the outbreak spreads.

There is concern in the US that the government is not handling the outbreak appropriately. Mixed messaging and an inadequate supply of testing kits came as the number of coronavirus cases in the US topped 500 over the weekend. President Trump retweeted a meme of himself fiddling on Sunday, drawing a comparison to the Roman emperor Nero who fiddled as Rome burned around him. This is a time when leadership is of paramount importance.

Borrowing costs are falling sharply–a silver lining for first-time homebuyers. The best advice for investors is not to panic. This, too, shall pass, although no one knows when.

General Robyn McLean 4 Mar

Canada has responded! Full commentary by DLC’s Chief Economist, Dr. Sherry Cooper

|

|